What is the difference between pre-approval and pre-qualification?

The pre-approval process is more complete than pre-qualification. For pre-qualification, the loan officer asks you a few questions and provides you with a pre-qual letter. Pre-approval includes all the steps of a full approval, except for the appraisal and title search. Pre-approval can put you in a better negotiating position, much like a cash buyer.

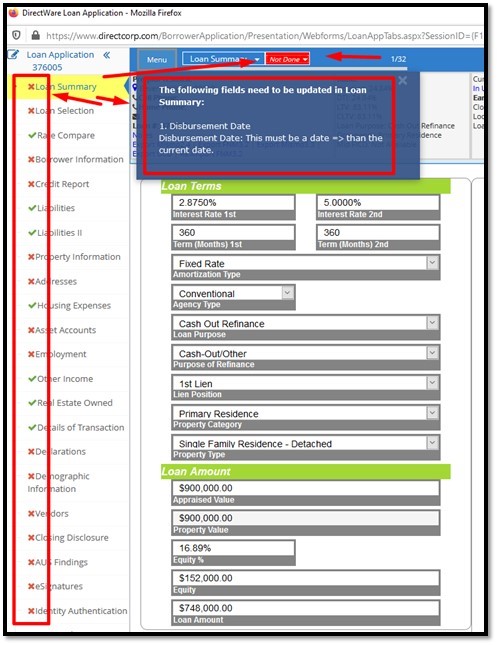

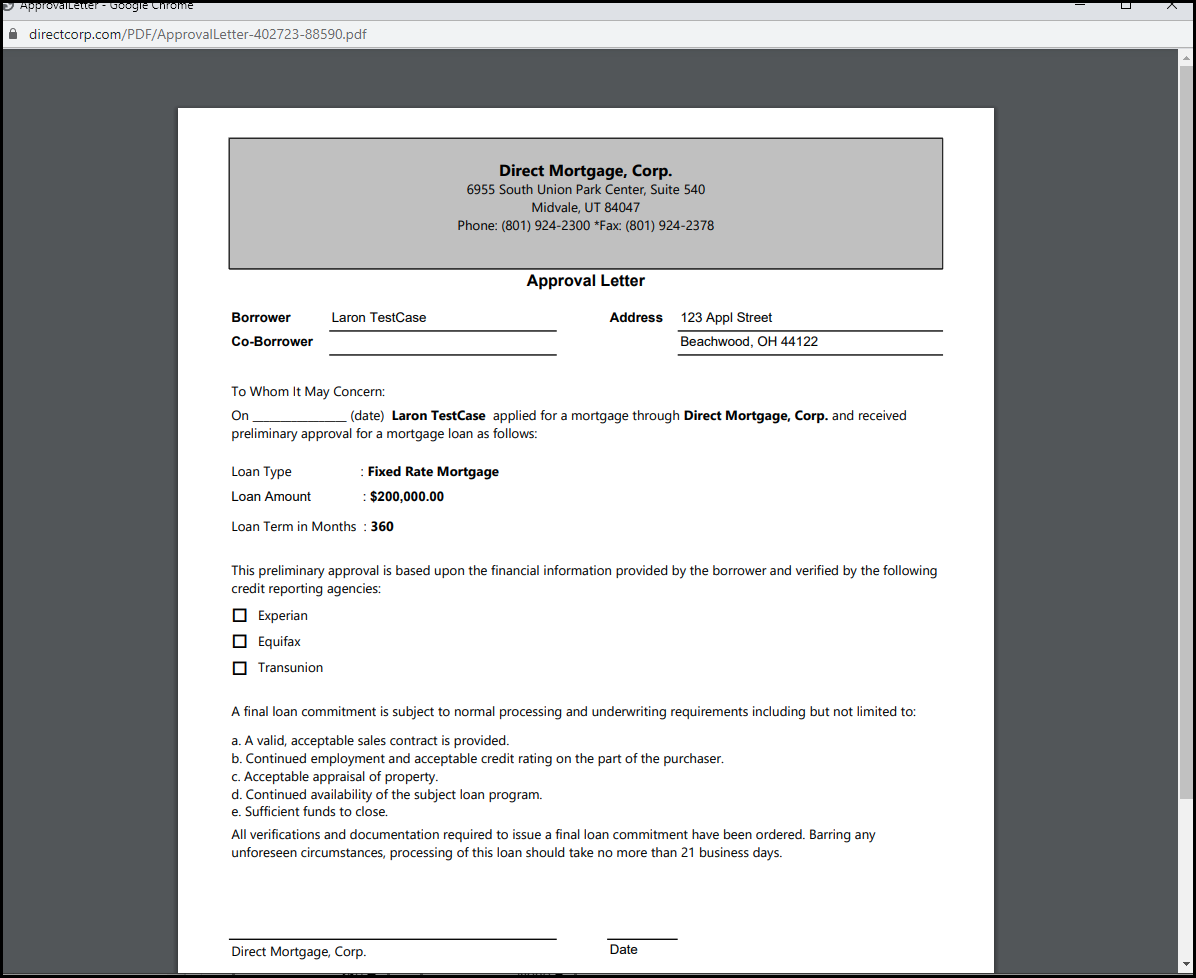

How do I print a Approval Letter? Direct Mortgage, Corp. assists with pre-approval utilizing its own DirectWare® software solution.

1. First, complete the pages to change the Incomplete Red X Check Marks to the Completed Green Check Marks on the loan application left side navigation links – from the Loan Summary page down through and including the Identity Verification page. Notice the “Not Done†function in the loan application header area. Click that to see what needs attention.

2. Next print the Approval Letter. This can be printed before completing the loan application steps, but be careful to not mislead the borrower with incomplete information. See the screenshot below for how to follow this click path:

Loan Application —> Loan Pulse Header Area —> Print Forms —> Search Box (type in a partial word search) —> click the Approval Letter report —> Save or print the PDF Approval Letter.

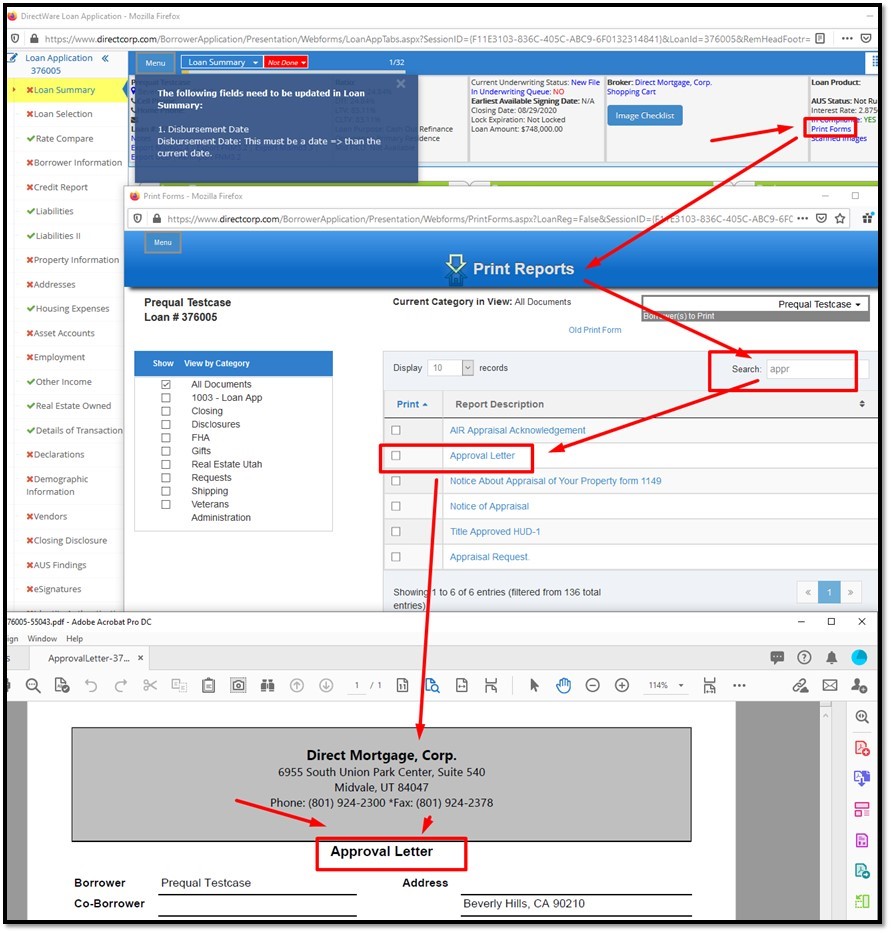

3. Queues for Active Loans; Prospect Loans; used for Prequalification and Pre-Approval.

a. Active loans have the obtained the required 6 data fields:

i. Borrower Names.

ii. Borrower Income.

iii. Borrower Social Security Numbers.

iv. Subject Property Address.

v. Property Value.

vi. Loan Amount.b. All Loans that obtain the required 6 data fields must be disclosed within 3 days or they will be automatically withdrawn. Loans withdrawn

because they were not disclosed within legal requirements cannot be reinstated (a new loan application must be restarted).

c. Prospect Loans are missing one or all of these required 6 data fields.

d. Access these queues from the Landing Page – shown in this screenshot.

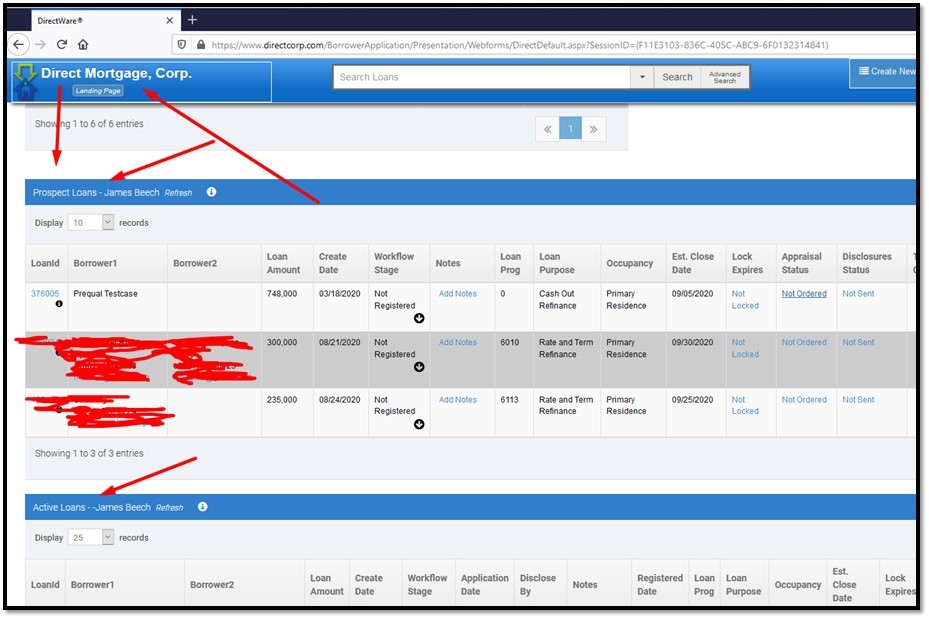

4. You can customize your loan queues through your settings. Here is the screenshot of how to access that.

Landing Page —> Click where your name is displayed in the header area —> Settings —> Display Queue.

This post was last updated on 9/01/2020.Â

When does it make sense to refinance?

Usually people refinance to save money, either by obtaining a lower interest rate or by reducing the term of the loan. Refinancing is also a way to convert an adjustable loan to a fixed loan or to consolidate debts. The decision to refinance can be difficult, since there are several reasons to refinance. However, if you are looking to save money, try this calculation:

Calculate the total cost of the refinance

Calculate the monthly savings

Divide the total cost of the refinance (#1) by the monthly savings (#2). This is the “break even†time. If you own the house longer than this, you will save money by refinancing.

Since refinancing is a complex topic, consult a mortgage professional.

This post was last updated on 9/01/2020.Â

What is the difference between a mortgage broker and a lender?

A mortgage broker counsels you on the loans available from different wholesalers, takes your application, and usually processes the loan which involves putting together the complete file of information about your transaction including the credit report, appraisal, verification of your employment and assets, and so on. When the file is complete, but sometimes sooner, the lender “underwrites†the loan, which means deciding whether or not you are an acceptable risk.

This post was last updated on 9/01/2020.Â

Will I save money going directly to a mortgage lender?

Mortgage brokers perform functions that still need to be done by employees of the lender. Working directly with a lender will create savings when the same tasks are required to be done by both the lender and the broker. Alternately, because mortgage brokers deal with multiple lenders, they can shop for the best terms available. They might also find lenders who specialize in various market niches that many other lenders avoid, such as loans to applicants with poor credit ratings, loans to borrowers who do not intend to occupy the property, or loans with minimal or no down payment. But sometimes these specialized loan products are not available to brokers, which will make more sense to work directly with a lender.

This post was last updated on 9/01/2020.Â

What is a full documented loan?

Both income and assets are disclosed and verified, and income is used in determining the applicant’s ability to repay the mortgage. Formal verification requires the borrower’s employer to verify employment and the borrower’s bank to verify deposits. Alternative documentation, designed to save time, accepts copies of the borrower’s original bank statements, W-2s and paycheck stubs.

This post was last updated on 9/01/2020.Â

What is a conforming loan?

A conforming loan is a mortgage that is equal to or less than the dollar amount established by the limit set by the Federal Housing Finance Agency (FHFA) and meets the funding criteria of Freddie Mac and Fannie Mae. For borrowers with excellent credit, conforming loans are advantageous due to lower Mortgage Insurance (MI) rates.

Fannie Mae and Freddie Mac are restricted by law to purchasing single-family mortgages with origination balances below a specific amount, known as the “conforming loan limit.†Loans above this limit are known as jumbo loans. Click the links below to access the current year conforming loan limits.

2020 Conforming Loan Limits

[XLS], [PDF], [MAP], [ADDENDUM]

This post was last updated on 9/01/2020.Â

What is a jumbo mortgage?

A jumbo loan, also known as a jumbo mortgage, is a type of financing that exceeds the limits set by the Federal Housing Finance Agency (FHFA). Unlike conventional mortgages, a jumbo loan is not eligible to be purchased, guaranteed, or securitized by Fannie Mae or Freddie Mac. Designed to finance luxury properties and homes in highly competitive local real estate markets, jumbo mortgages come with unique underwriting requirements and tax implications. These kinds of mortgages have gained traction home prices increase.

The starting amount of a jumbo mortgage varies by state—and even county. The FHFA sets the conforming loan limit size for different areas traditionally on an annual basis.

This post was last updated on 9/01/2020.Â

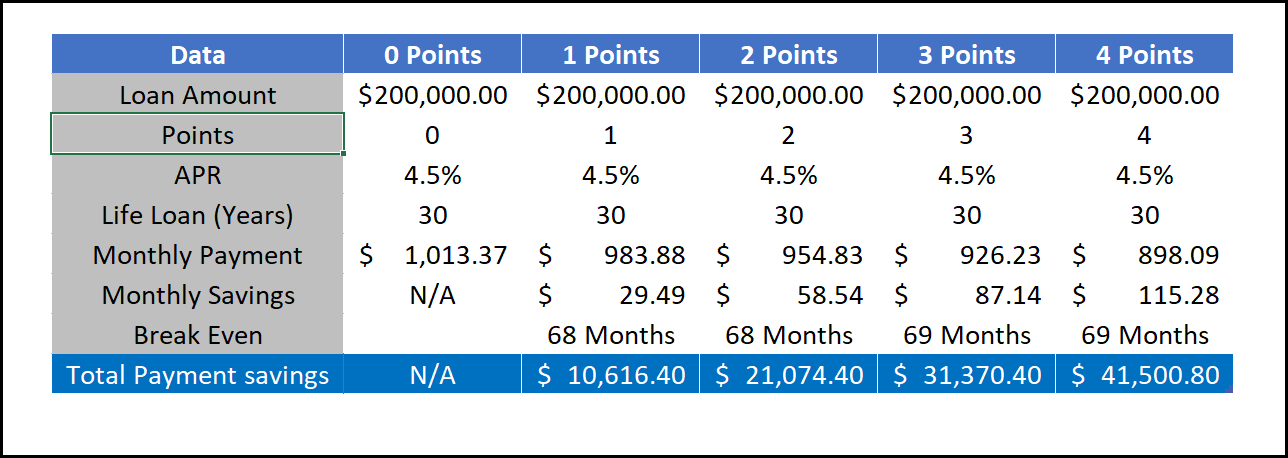

What are points?

Points are an upfront cash payment required by the lender as part of the charge for the interest rate, expressed as a percent of the loan amount; e.g., “2 points†means a charge equal to 2% of the loan balance.

Divide the points cost by the monthly savings to find the “break even†time. If you own the house longer than this, you will save money by paying points upfront.

See below for an example of how points work. In the example below the points represent a 0.25% reduction.

*Sample APRs and points are for educational purposes only and are not an actual quote or commitment to lend. Actual rate buydown per point varies by loan program and market conditions.

This post was last updated on 9/01/2020.Â

Do you allow FHA paying off a PACE lien as rate and term?

We follow all FHA guidelines. Below is a direct quote from their website as well as a link to their site for more information.

HUD Guidance on “PACE†Lending

![]() On July 19, the U.S. Department of Housing and Urban Development (HUD) released guidance stating the Federal Housing Administration (FHA) will insure mortgages on certain properties with Property Assessed Clean Energy (PACE) assessments. Properties with PACE obligations must meet strict criteria which are outlined below and can be found in the FHA release linked below.

On July 19, the U.S. Department of Housing and Urban Development (HUD) released guidance stating the Federal Housing Administration (FHA) will insure mortgages on certain properties with Property Assessed Clean Energy (PACE) assessments. Properties with PACE obligations must meet strict criteria which are outlined below and can be found in the FHA release linked below.

“While FHA loans represent approximately 20 percent of mortgage loans, the California Credit Union League continues to advocate for additional guidance from the Federal Housing Finance Agency, which continues a policy of not accepting mortgages with a super-priority PACE lien. The League will also continue to support AB 2693 and push for underwriting standards for PACE lenders from the Consumer Financial Protection Bureau,†said Courtney Jensen, League legislative advocate.

PACE loans continue to be unregulated, have no required underwriting standards, high interest rates, prepayment penalties, high administrative costs, no ability to repay standards, and put homeowners at a high risk. AB 2693—if approved by the California Legislature and signed by Governor Brown—would require California PACE lenders to provide a new truth-in-lending disclosure to consumers three days before they sign up for a PACE loan, and also provides for a three-day right to cancel. At the very least this will allow consumers clear information on what they are signing up for and give them time to understand the potential consequences of this type of loan.

- Under the new guidance, to qualify for FHA insurance on mortgages for properties that include PACE assessments, lenders must determine that the following requirements have been met:

- The PACE obligation must be collected (escrowed) and secured by the creditor in the same manner as a special assessment against the property

- The entire amount of the PACE obligation cannot become due in the event of delinquency after endorsement of the FHA-insured mortgage

- Only the delinquent portion of the PACE obligation is superior to the FHA-insured mortgage

- There are no terms or conditions that limit the transfer of the property to a new homeowner

- The existence of a PACE obligation on a property is readily apparent to mortgagees, appraisers, borrowers and other parties to an FHA-insured mortgage transaction, and information on PACE obligations must be readily available for review in public records

- In the event of the sale of the property with outstanding PACE financing, the PACE assessment remains with the property. (HUD Guidance)

For more information, click here.

This post was last updated on 9/01/2020.Â

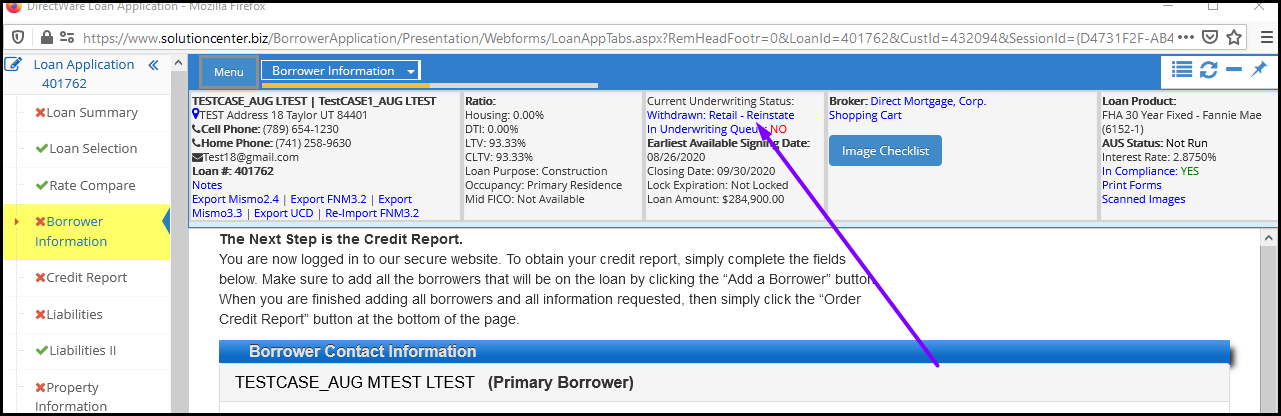

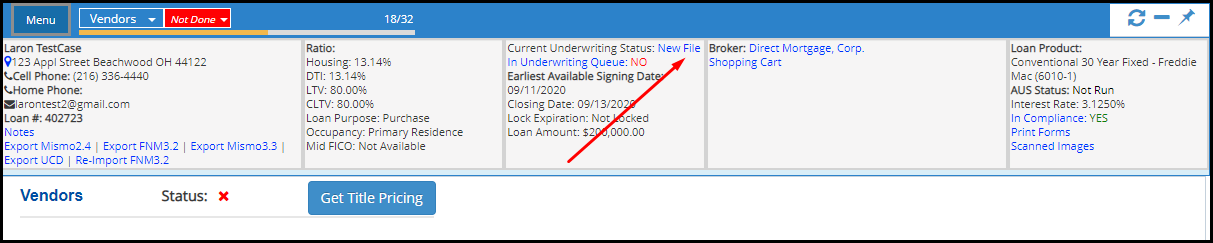

How can I check the underwriting status of a loan?

After logging into DirectWare:

1. Select the loan you wish to work on in the search Loans area of the Landing page header. You can search by loan number, by borrower first or last name (or use both), or use a partial name. There is also an “Advanced Search†option available to the right of the search box.

2. Once in a Loan Locate the Loan Pulse section at the top of the screen.

3. Look for the “Current Underwriting Status†field

This post was last updated on 9/08/2020.Â

Screenshot Instructions

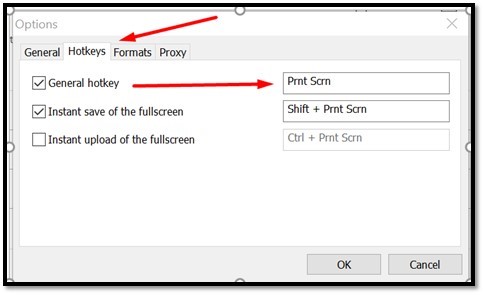

1. Install Lightshot (https://app.prntscr.com/en/index.html), right click on its icon in the system tray, and then choose “Optionsâ€.

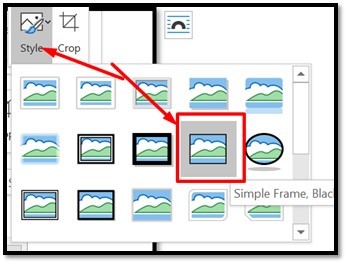

2. When you are done adding arrows and text, and boxes, then Click “CTRL+C†to copy, and then “CTRL+V†to paste it in an email or word document. Then “Right-Click†the image à then select “Style†– then choose the border frame.

3. To select a “Print Screen†Hotkey, see this screen shot. To use a different “hotkey†then place cursor in the text box, and click the key combination that you want to use. Then click “OKâ€.

This post was last updated on 9/01/2020.Â

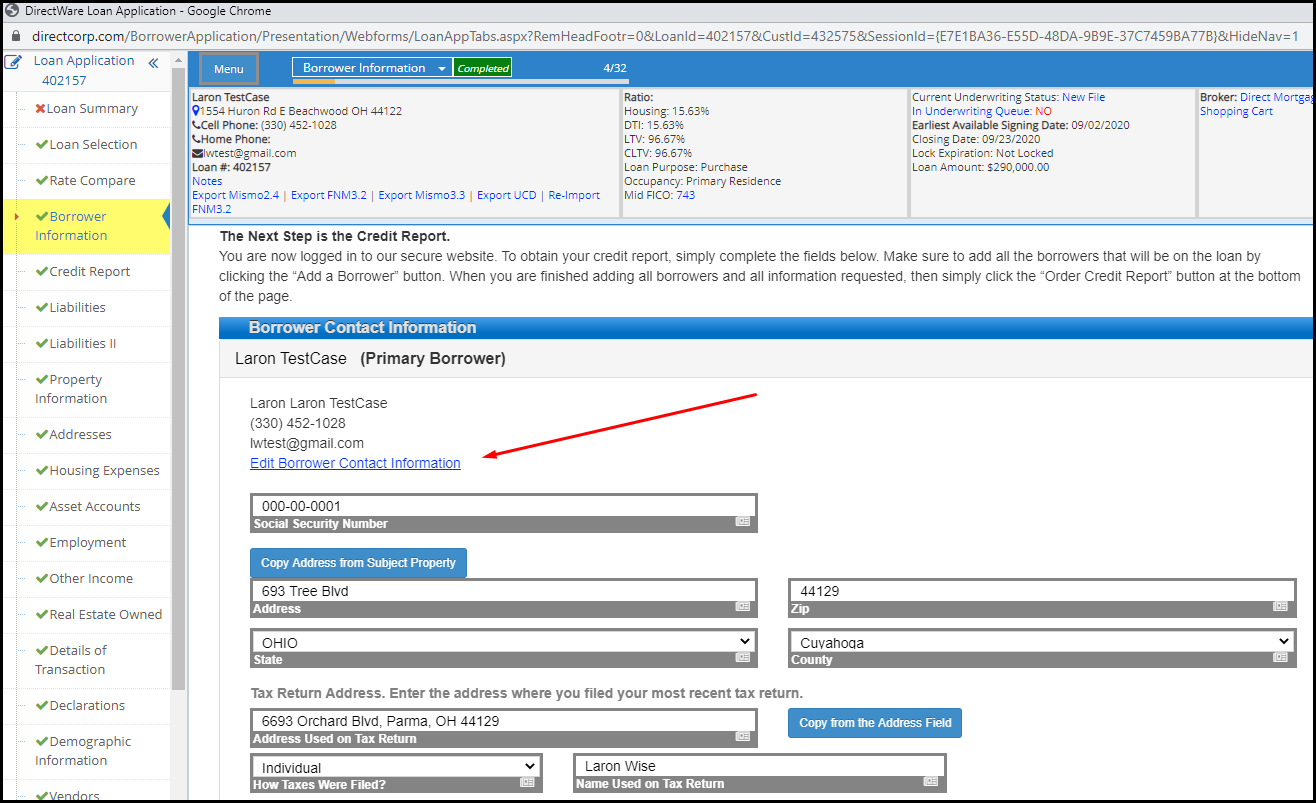

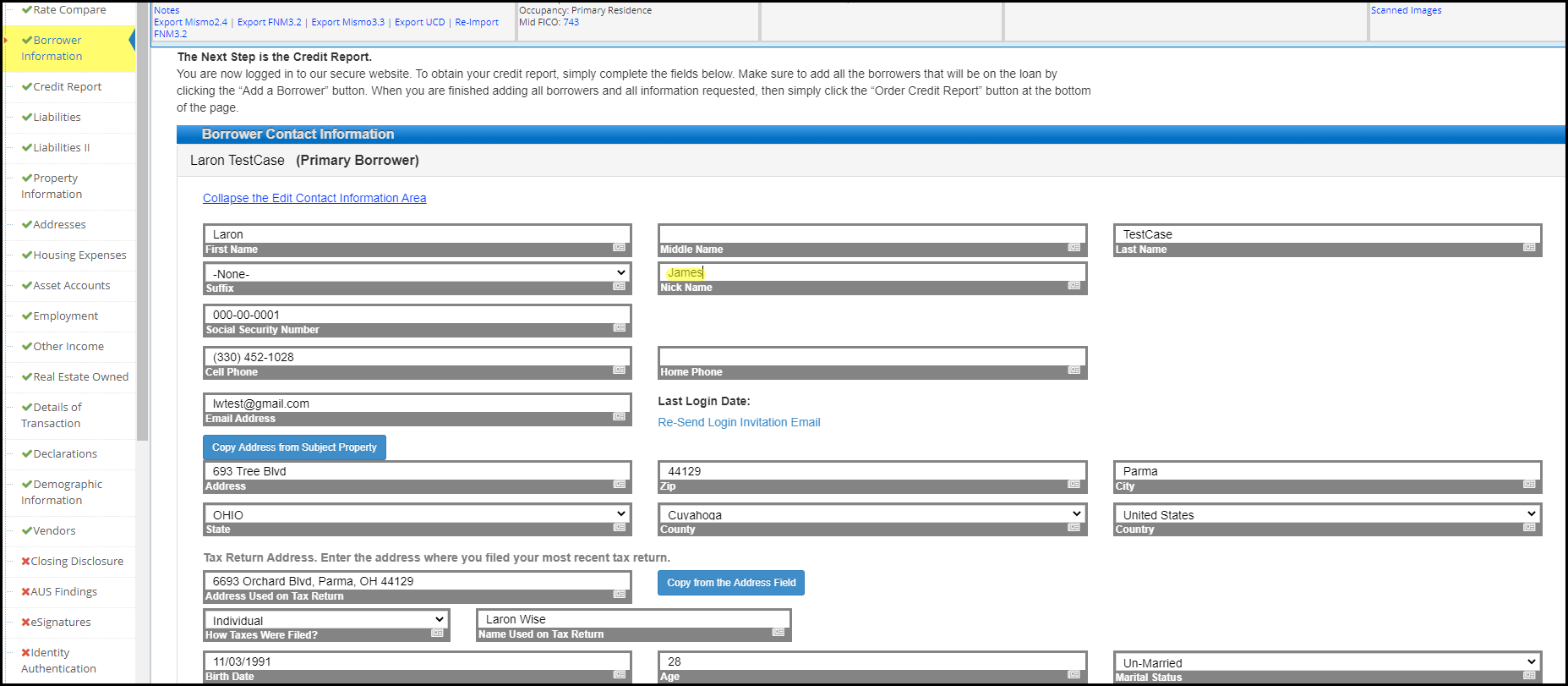

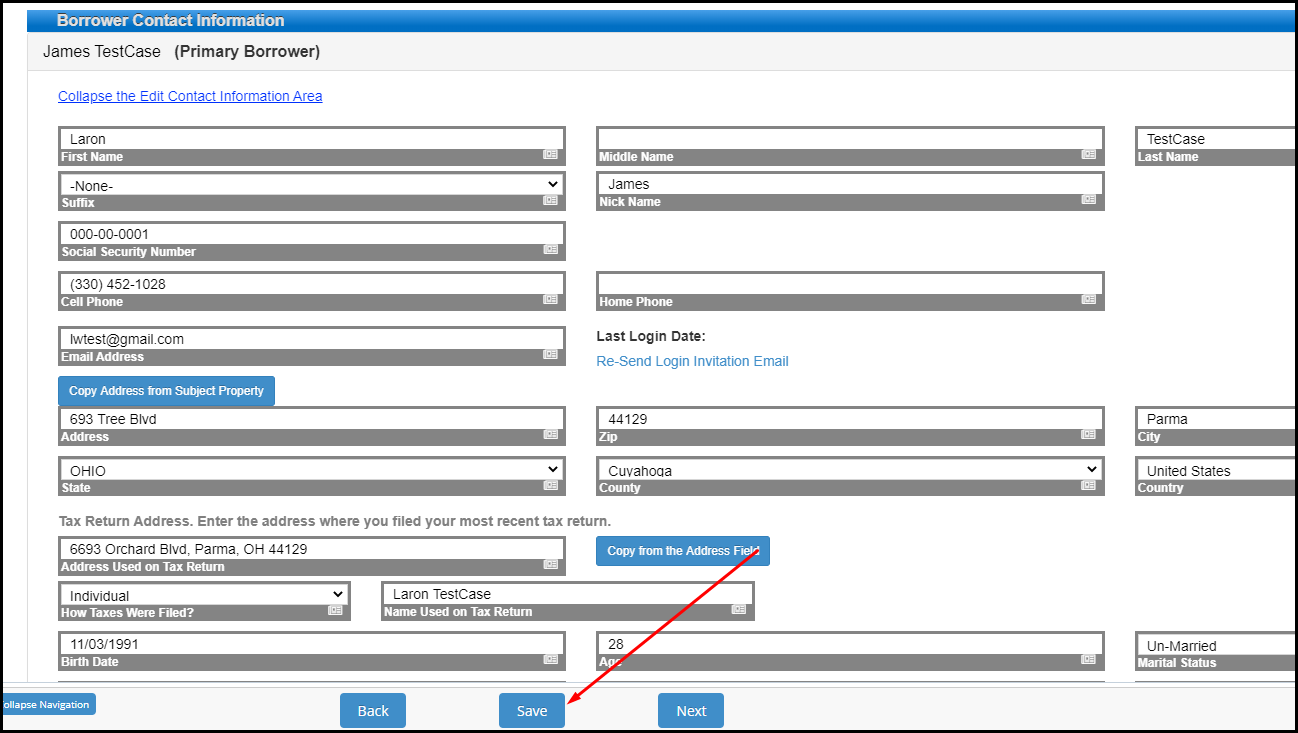

How do I update a borrower's address details?

1. After you’ve logged in and located the loan you want to change the information for click on Borrower’s Information on the left side menu.

2. Once the page loads click on the Edit Borrower’s Contact Information link.

3. There you will be able to edit any information you deem as necessary.

4. Once you’re done please be sure to click the save button at the bottom.

5. You may have to click the refresh button in the top right hand corner inside the header to see updates.

This post was last updated on 9/01/2020.Â

What if I am having technical difficulties?

Send an email to MakeMeAware@directcorp.com with as much detail as possible, including what you did leading up to the problem. Please include screenshots whenever possible.

This post was last updated on 9/01/2020.Â

Where can I view Direct Mortgage loan products?

Follow this link for a list of our loan products.

This post was last updated on 9/01/2020.Â

What if I have a question about a loan program?

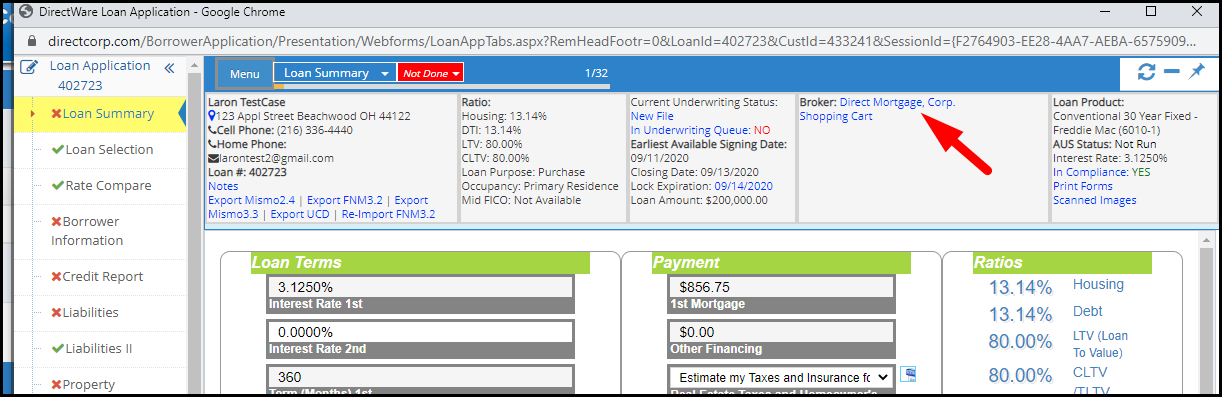

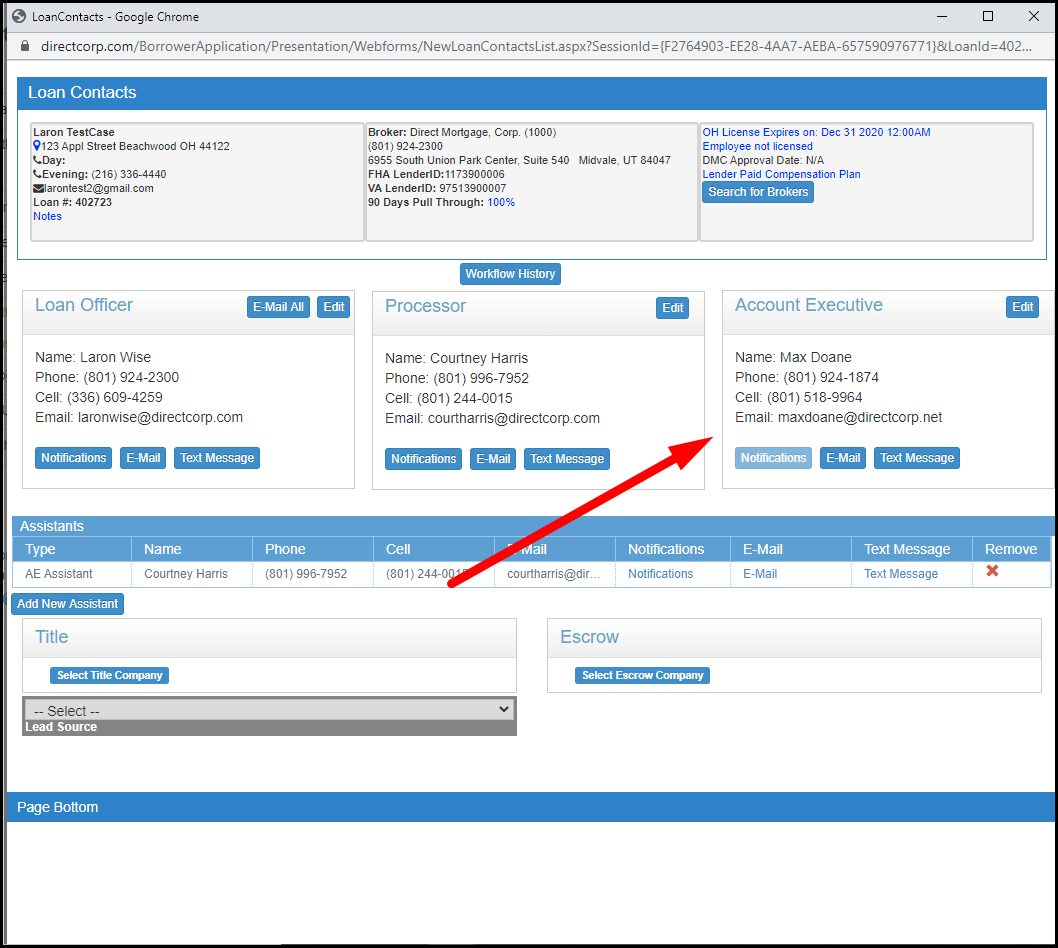

Your primary resources for information about loan programs are your Account Executive and our broker support team. If for some reason you still need additional clarification after talking with them, send an email to LoanInfo@directcorp.com with as much detail as possible. Below are screenshots on how to find your Account Executive (AE).

- Login and access any loan number then click on the Broker Name from the header area to access your Account Executive’s contact information.

- The following screenshots show an example on how to access your Account Executive’s contact information.

This post was last updated on 9/03/2020.Â

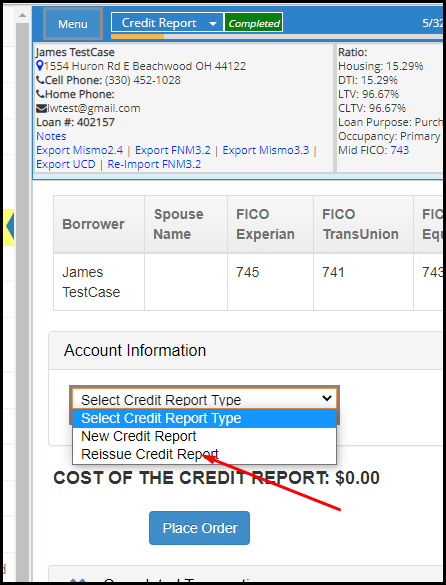

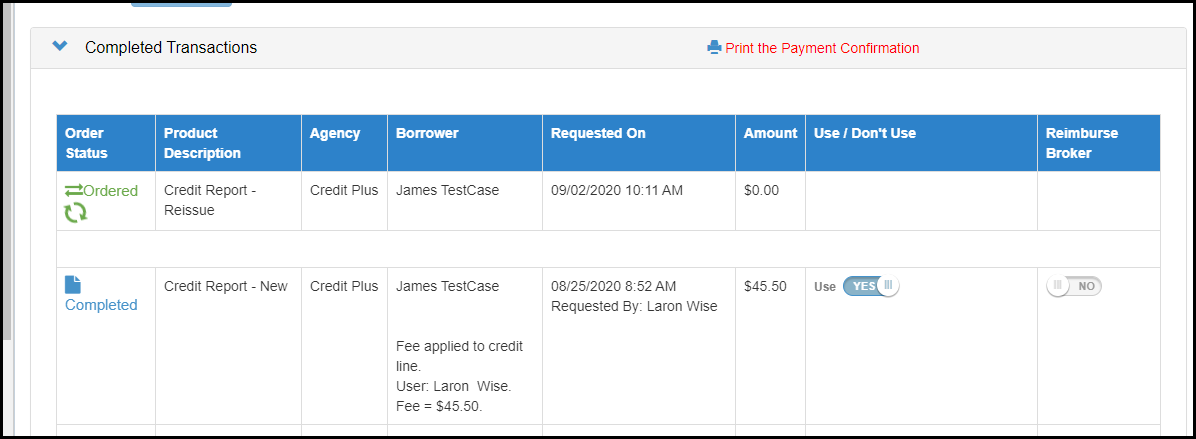

Can I reissue, re-pull, or input credit reports?

1. Log into DirectWare® at www.DirectCorp.com/Sitelogin/

2. Select the loan you wish to work on in the search Loans area of the Landing page header. You can search by loan number, by borrower first or last name (or use both), or use a partial name. There is also an “Advanced Search†option available to the right of the search box.

3. When the loan opens click on the Credit Report page on the left hand side.

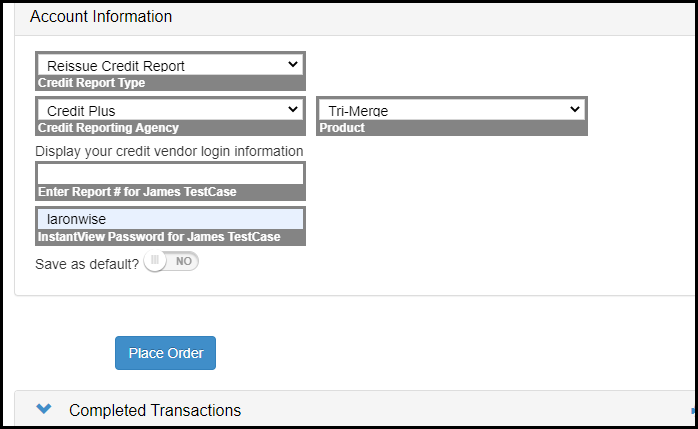

4. From the top dropdown field, choose whether or not you want to order a new credit report or reissue a credit report.

5. Select the reporting agency of the credit report you already have – from the Credit Reporting Agency drop down menu.

Note: Only vendors shown in our drop down are approved agencies. If your credit agency isn’t found, then please order a new credit report from our drop down, or directly from one of our approved credit reporting agencies.

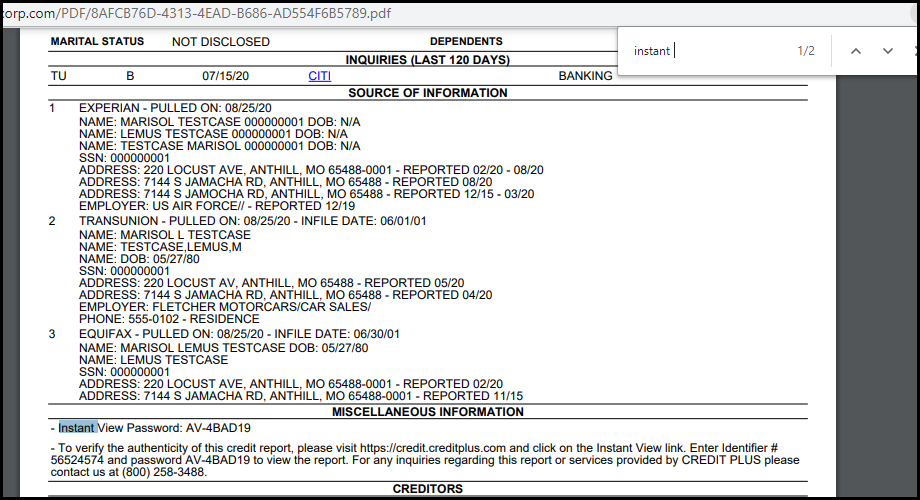

6. Enter your login credentials from your credit reporting agency (do not use your DirectWare login ID). Also, enter the Report #. And any additional information requested – like the InstaView Password. If you mark the check box, text boxes will appear where you can enter you login information. Below is an screenshot example of where to find the Credit Report # and Instant View password from your credit report.

7. The shopping cart (Completed Transactions area) shows “Credit Report – Reissue†for zero dollars. If you want the amount you paid for the credit report to be added to the Closing Disclosure from this screen, then simply check the “Reimburse Broker†swatch.

8. The status under the “Order Status†column will change from “Orderedâ€, to “Completedâ€. Click on the “Ordered†link to open the “Order Status†screen. Click on the “Completed†link to open the credit report. You can also open the credit report from the loan pulse area at any time by clicking on the Mid FICO score.

9. The credit report data is now successfully imported, and the debt liabilities are ready for review on the Liabilities screen.

This post was last updated on 9/11/2020.Â

How can I see your rates?

You can request to be added to our daily rates email.

If you are an EXISTING Direct Mortgage user – Login here and then Select the desired Rate Sheets in your Email Subscription Preferences screen.

If you are a NEW user to Direct Mortgage – Click here to Sign up – after creating your login navigate to the Email Subscription Preferences screen.

This post was last updated on 9/02/2020.Â

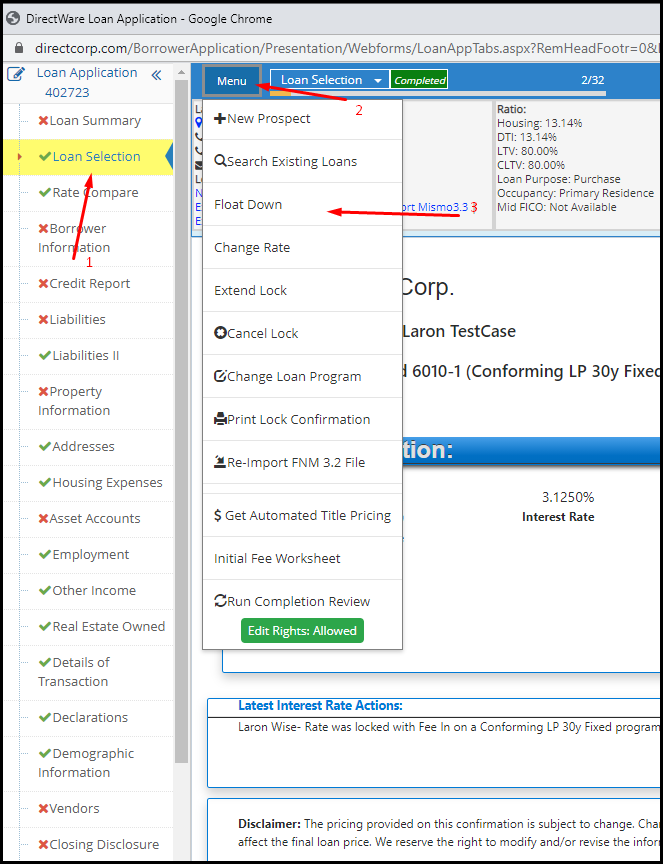

Do you offer rate float downs?

Interest rate float downs are available with most of our mortgage loan products. Simply click the Float Down option found in the Menu button at the top and bottom of the lock confirmation screen.

1. Log in

2. Select the loan you wish to work on in the Search Loans area of the Landing page header. You can search by loan number, by borrower first or last name (or use both), or use a partial name. There is also an “Advanced Search†option available to the right of the search box

3. You will be taken to “Loan Selection†>> Click “Menuâ€Â >> click the “Float Down†button

4.  Select your new rate and Lock Period >> click “Saveâ€

.

Rate Float Down Policy

A one-time float down option may be available for locks in which the price has improved, and are subject to the following conditions:

- Float Down must be done before the loan receives final underwriting approval and the loan is approved for docs.

- Loan must be within 10 days of funding. (If the lock expiration is not within 10 days, a float down may be granted if the lock expiration is moved to 10 days from the date of the float down.)

- Loan must close and fund by the original lock expiration date

- Loan program and term must be the same as the original loan program and term at time of lock

- Price will be improved to current market price plus a float down adjustment, for pricing of the same lock period as the original lock period. For example, if the loan was originally locked on a 30 day price, the current 30 day price will be used to determine the price after the float down option has been exercised. The float down adjustment may vary by loan program. If a loan has been previously been extended, the extension cost will be added to the new price.

- Loan Program Changes are allowed after the float down option has been exercised, and the price will be determined by our current policy for changing loan programs*. If a loan has been previously extended, the extension cost and the float down adjustment will be added to the new price.

- Lock Extensions are allowed after the loan has been floated down as long as the loan has not been previously extended. Only one extension per loan is allowed.

Exceptions to the above conditions may be considered by the price desk. Exception requests should be submitted in writing, by the Loan Officer through the Account Executive assigned to your account. (DMC reserves the right to withhold the Float Down programs).

* Requests to change the loan program of a current lock may be granted at the worst of the original lock price or current lock price, when available. As market conditions dictate, an additional market adjustment may be charged.

This post was last updated on 9/02/2020.

Do you offer jumbo loans?

Yes. View a complete list of our wholesale mortgage loan products.

This post was last updated on 9/01/2020.Â

How do I add loan officers & Processors (and other user types)?

This is fast and easy. Complete the online user signup wizard found here: User Sign Up Wizard.

If your company has previously been approved with us, make sure your new user searches diligently to Associate With Your Company at the required company step (otherwise they will create a new company and their approval will be delayed). Your own login admin can approve these new user requests in their own task list on their Home Landing Page.

Also see the FAQ: How do I become approved with Direct Mortgage, Corp.?

This post was last updated on 9/01/2020.Â

How do I become approved with Direct Mortgage, Corp.?

This is fast and easy. Complete the online signup wizard found here: User Sign Up Wizard.

You can begin locking interest rates and submitting loan files immediately. Broker approval can be processed during your first loan submission, but is often not necessary because the formal approval is typically done well before that.

Also see the FAQ: How do I add loan officers & processors (and other user types)?

This post was last updated on 9/01/2020.Â

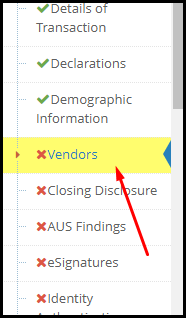

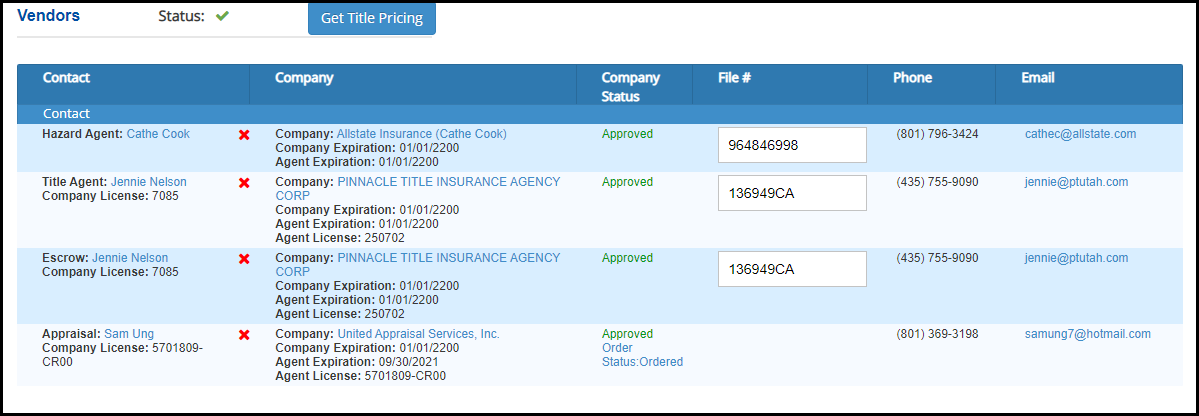

How do I find the hazard insurance of a loan?

1. Select the loan you wish to work on in the search Loans area of the Landing page header. You can search by loan number, by borrower first or last name (or use both), or use a partial name. There is also an “Advanced Search†option available to the right of the search box.

2. Once the loan page opens click on vendors from the side menu

3. Check the “Current Underwriting Status†in the header. Please note there will be no insurance premium paid to the vendor until after the loan closes.

4. From the Vendors page you can see who the hazard insurance vendor was “supposed to beâ€. Verify the information is correct. Don’t change anything, because the loan officer or processor are normally the one that should update the hazard vendor.

This post was last updated on 9/03/2020.Â

How do I become approved with Direct Mortgage, Corp.?

This is fast and easy. Complete the online signup wizard found here: User Sign Up Wizard.

You can begin locking interest rates and submitting loan files immediately. Broker approval can be processed during your first loan submission, but is often not necessary because the formal approval is typically done well before that.

Also see the FAQ: How do I add loan officers & processors (and other user types)?

This post was last updated on 9/01/2020.Â

How do I add loan officers & processors (and other user types)?

This is fast and easy. Complete the online user signup wizard found here: User Sign Up Wizard.

If your company has previously been approved with us, make sure your new user searches diligently to Associate With Your Company at the required company step (otherwise they will create a new company and their approval will be delayed). Your own login admin can approve these new user requests in their own task list on their Home Landing Page.

Also see the FAQ: How do I become approved with Direct Mortgage, Corp.?

This post was last updated on 9/01/2020.Â

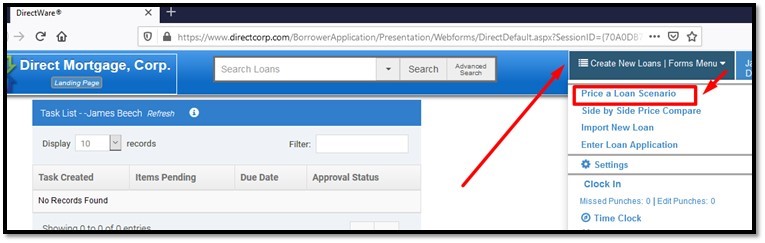

How do I price a loan scenario?

Interest Rates and Loan Product scenarios are priced using our DirectWare® website.

The click path is DirectWare Landing Page —-> Create New Loans | Forms Menu —–> “Price a Loan Scenarioâ€.

This post was last updated on 9/01/2020.Â

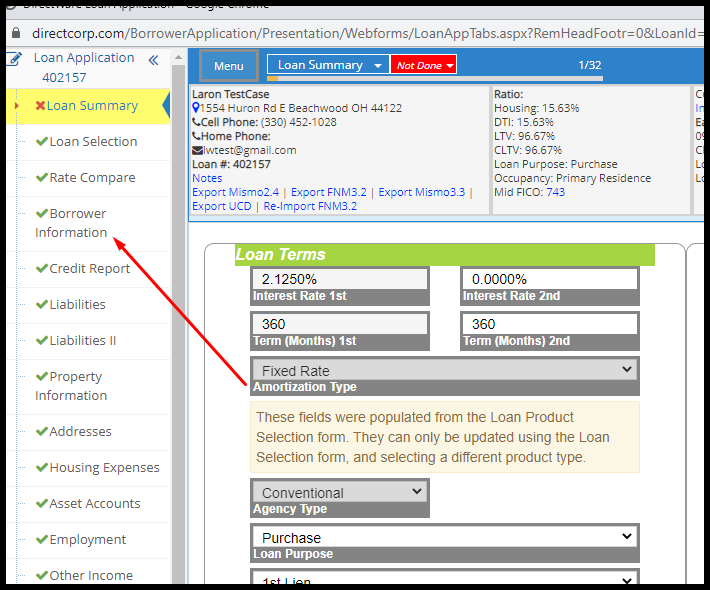

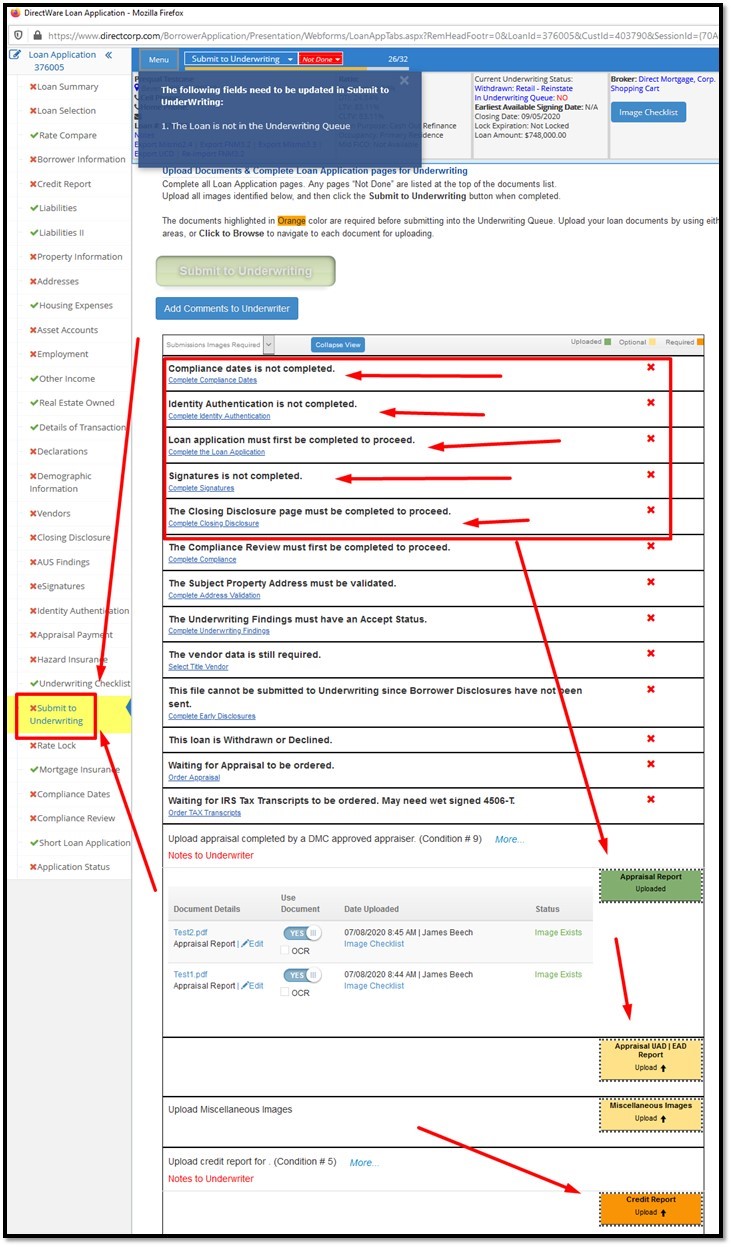

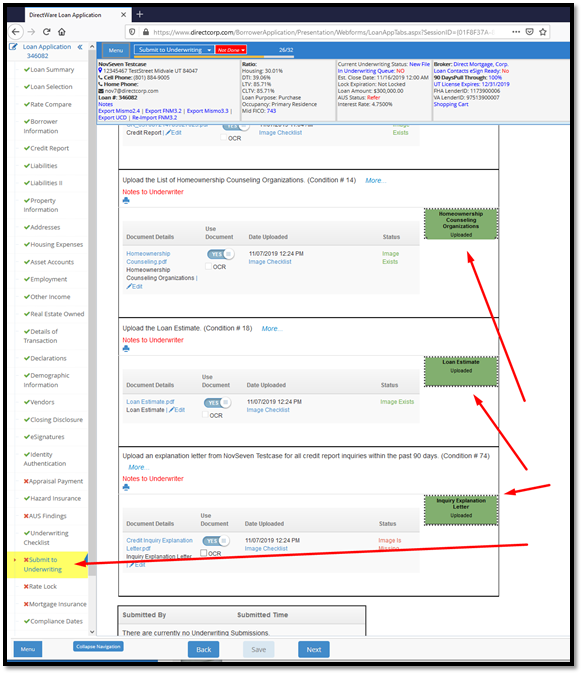

How do I submit loan files to underwriting?

Loan files are uploaded at the Submit to Underwriting step in the loan application (see the screen shot). Best practices are:

1) Follow the Left Hand Navigation. Turn all Red X’s into Green Checkmarks by completing each page.

2) If a page is “Not Done†then click the Red “Not Done†area in the header to see what is incomplete or missing.

3) When viewing the Submit to Underwriting page, simply upload the required documents listed in the Orange background. Other documents have either been uploaded (Green Background), or are optional to complete that current submission step. Optional images are often better to upload sooner rather than later – to experience a faster underwriting turn time.

Here is what the Submit to Underwriting Screen looks like:

This post was last updated on 9/01/2020.Â

What states are you available to lend in?

Direct Mortgage is able to fund mortgage loans in many states across the country. Click here to view our current list: Direct Mortgage Licensed States.

Here’s the link. (https://www.directcorp.com/licensing/)

This post was last updated on 9/01/2020.Â

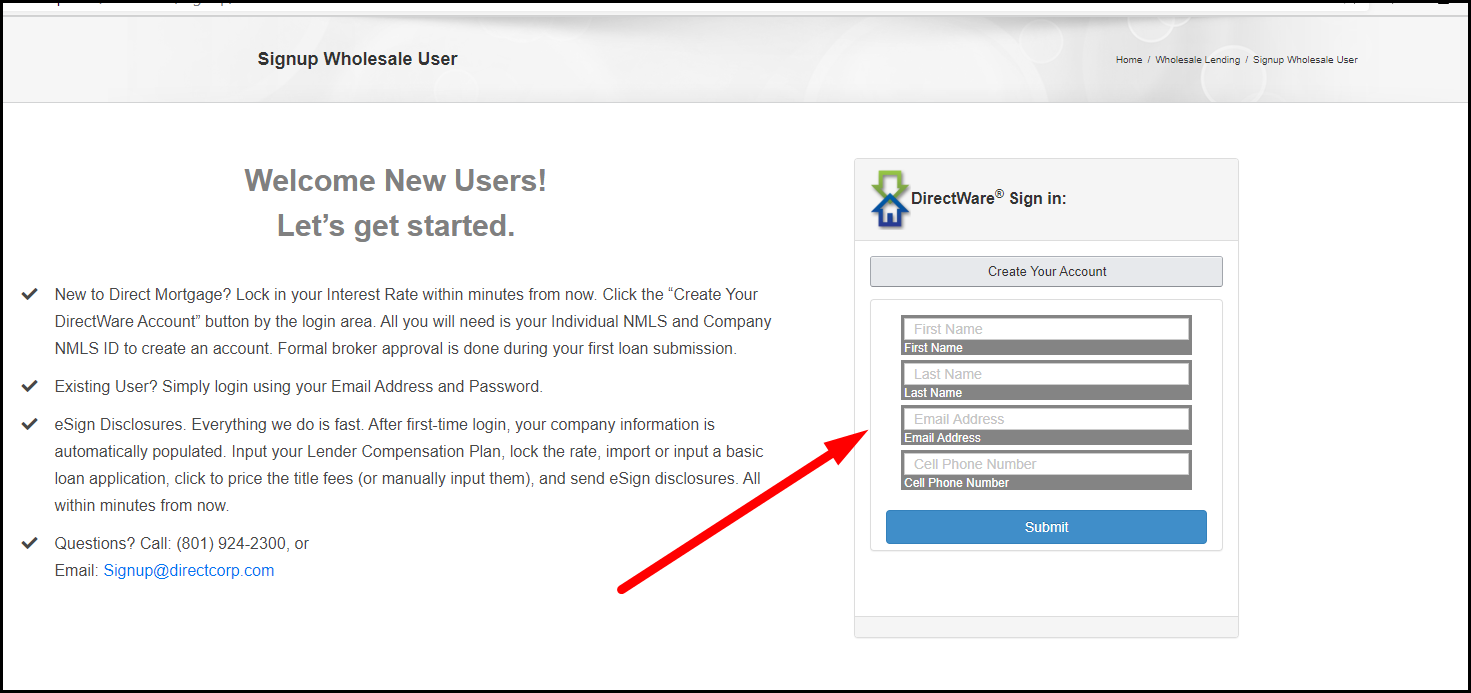

I don't have a login. How can I get one?

To obtain a login is fast and easy. Complete the online user signup wizard found here: User Sign Up Wizard.

If your company has previously been approved with us, make sure your new user searches diligently to Associate With Your Company at the required company step (otherwise they will create a new company and their approval will be delayed). Your own login admin can approve these new user requests in their own task list on their Home Landing Page.

We’ve included below what the Create an Account screen looks like for your reference.

Also see the FAQ: How do I become approved with Direct Mortgage, Corp.

This post was last updated on 9/03/2020.Â

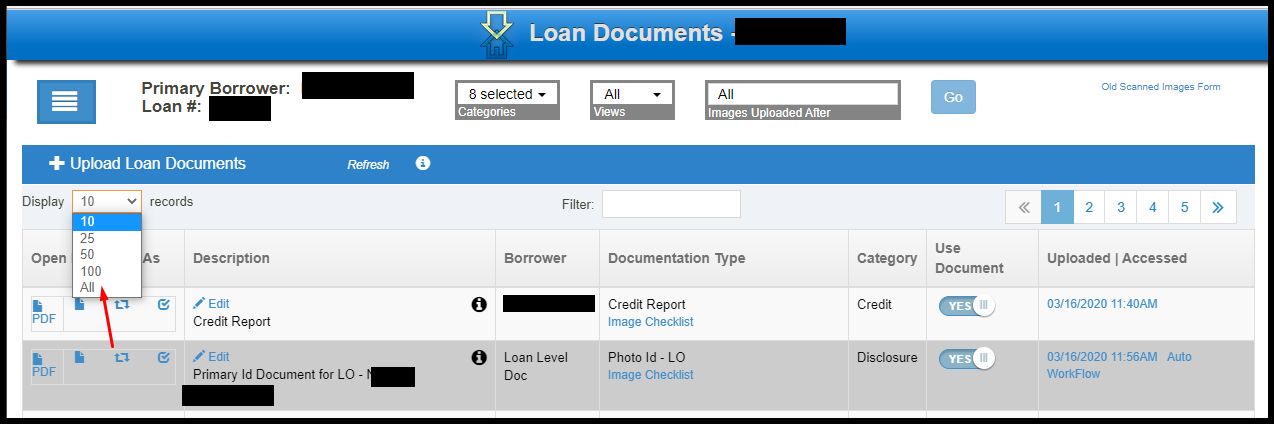

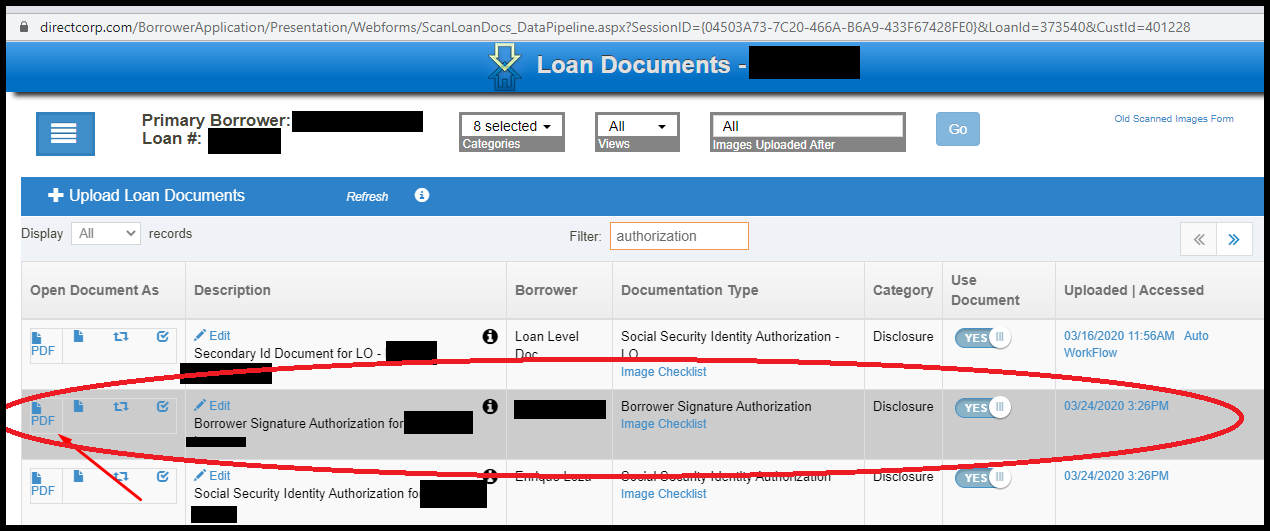

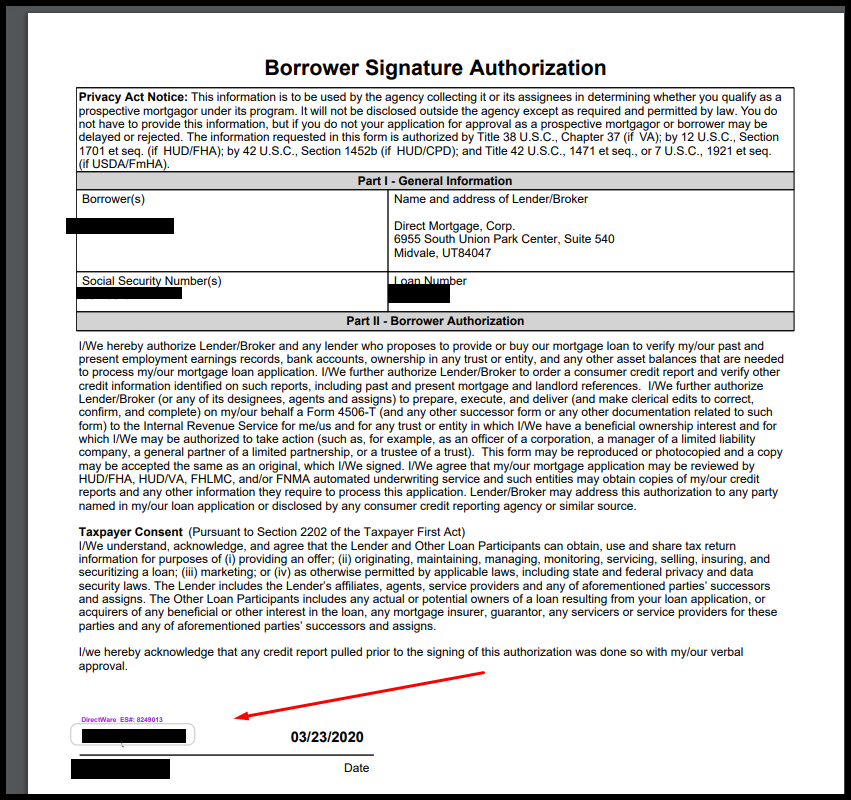

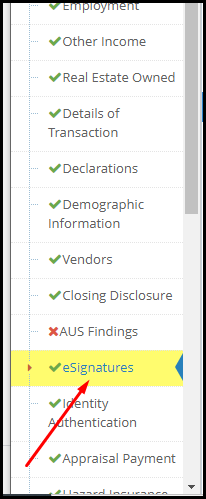

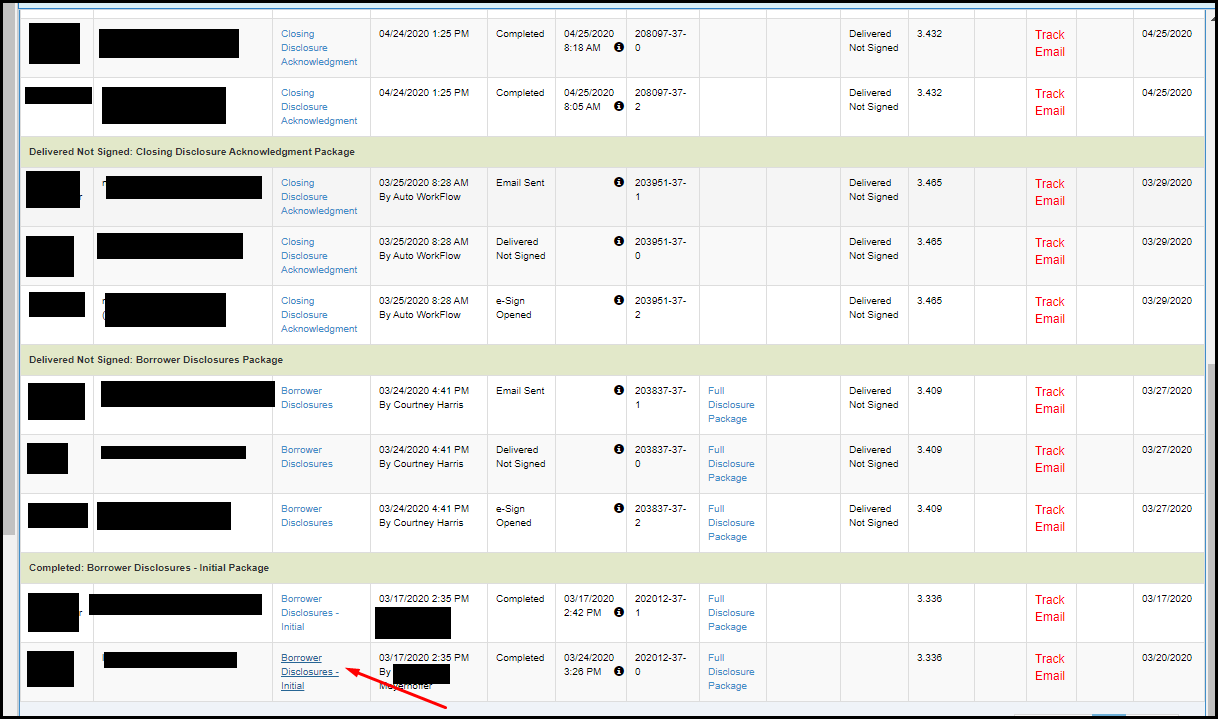

How do I find a borrower's signature authorization?

You can find a borrower’s signature authorization in two ways. I have included the steps below as well as screenshots to better depict the process.

Method # 1

1. Select the loan you wish to work on in the search Loans area of the Landing page header. You can search by loan number, by borrower first or last name (or use both), or use a partial name. There is also an “Advanced Search†option available to the right of the search box.

2. Once the loan file opens you can look for the “Scanned Images†hyperlink in the upper right hand corner

3. Be sure to change the display to all records

4. The fastest way to find the form is to use the filter and type in “authorization†then click the PDF hyperlink next to the file you are looking for.

5. After clicking the hyperlink a new window should open to show the form. If the window does not open be sure to have pop ups enable on this page.

Method # 2

1. Access the Loan Number from the Search or Recent Loans List

2. Once the Loan Page opens you want to click on the ESignatures hyperlink

3. From there you need to find the borrower’s disclosures hyperlink. Please note that each color of the bar represent a different document status. (Green = Complete, Orange = “xâ€, Red = “Xâ€, & Brown = Incomplete)

4. After clicking the link a new page should open and you can find the authorization page by using “Ctrl+F†and typing in “authorization†until you find the page (usually around page 10-13).

This post was last updated on 9/08/2020.Â

How do I find out who my AE (account executive) is?

To find your Account Executive you can find their contact information within any loan file, or contact our support at MakeMeAware@directcorp.com or (801)-924-2300 and ask who your Account Executive (AE) is. Here are the instructions to find the Account Executive (AE) in any loan file.

- Login and access any loan number then click on the Broker Name from the header area to access your Account Executive’s contact information.

- The following screenshots show an example on how to access your Account Executive’s contact information.

This post was last updated on 9/03/2020.Â

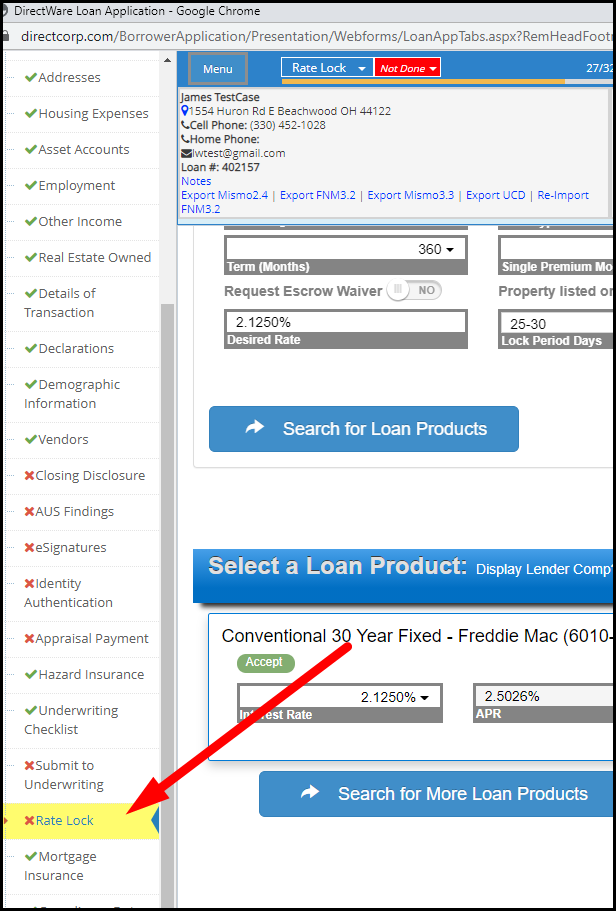

What is a rate lock?

A rate lock is a contractual agreement between the lender and buyer.

There are four components to a rate lock:

- Loan Program

- Interest Rate

- Points

- The length of the lock

You can find information on the rate locks from the side menu once you’ve opened a loan which is depicted in the screenshot below.

This post was last updated on 9/09/2020.Â

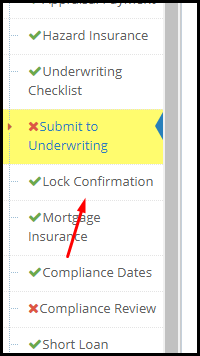

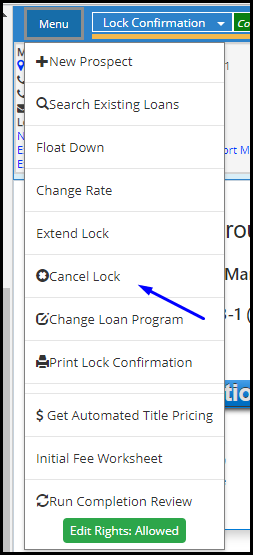

How do I cancel a lock?

After logging into DirectWare:

1.  Select the loan you wish to work on in the search Loans area of the Landing page header. You can search by loan number, by borrower first or last name (or use both), or use a partial name. There is also an “Advanced Search†option available to the right of the search box.

2. After opening the loan look to the side menu and find Lock Confirmation then click it.

3. Once the page loads locate the thumb menu on the loam page towards the header.

3. Once the menu opens click on Cancel Lock and leave whatever notes are necessary.

Also follow this link to view our rate lock policies and procedures here.

This post was last updated on 9/09/2020.Â

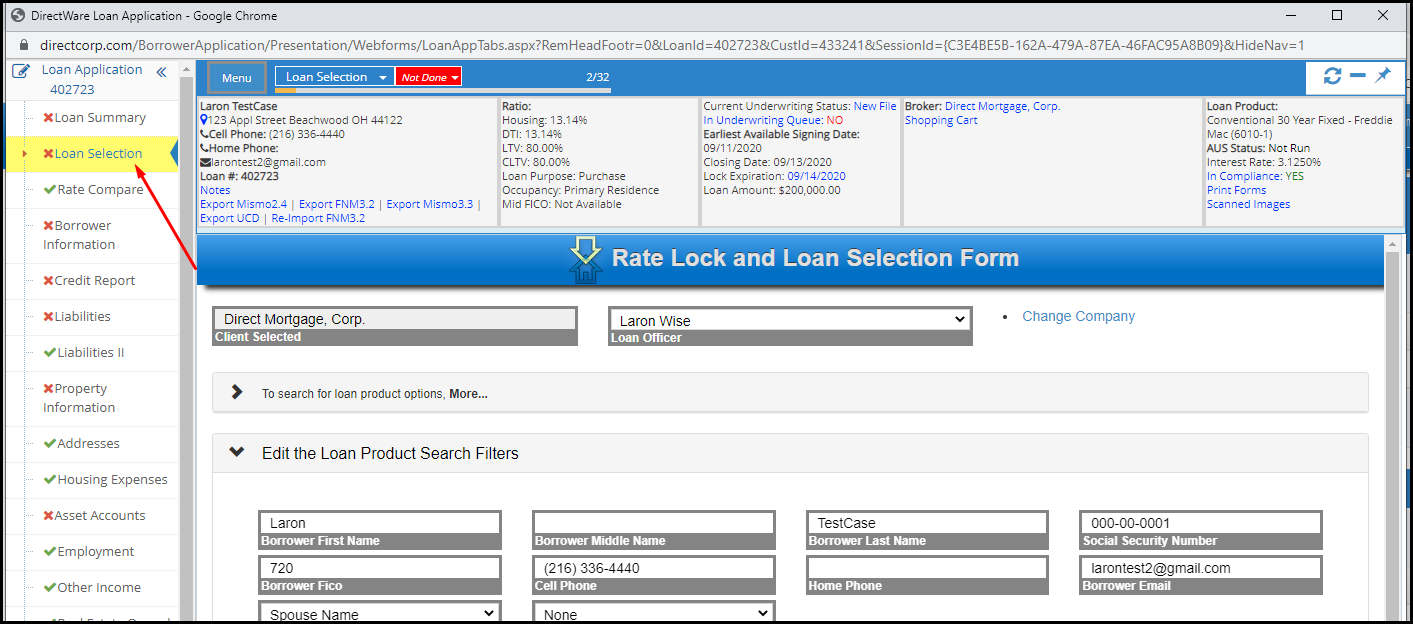

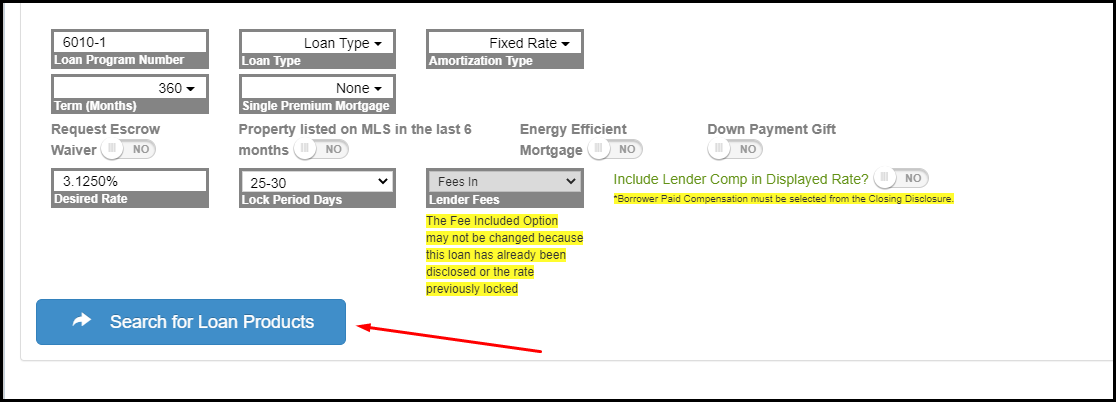

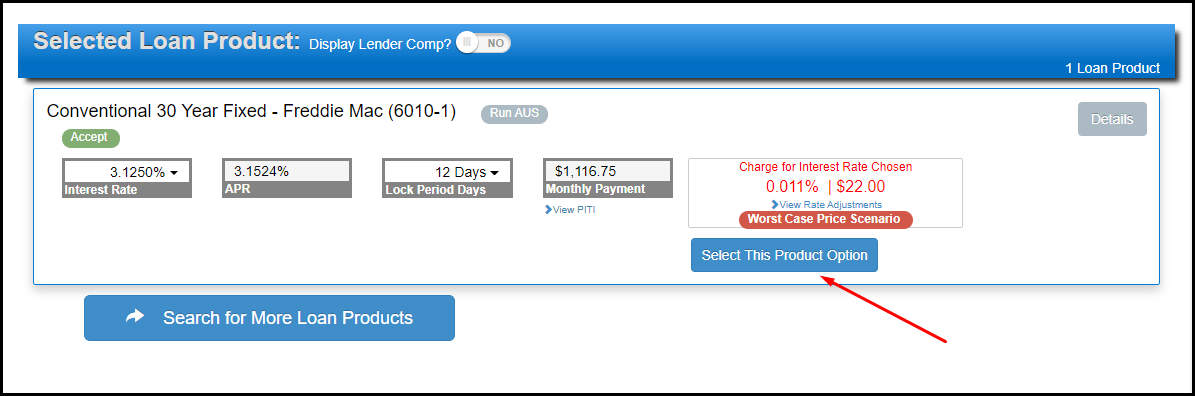

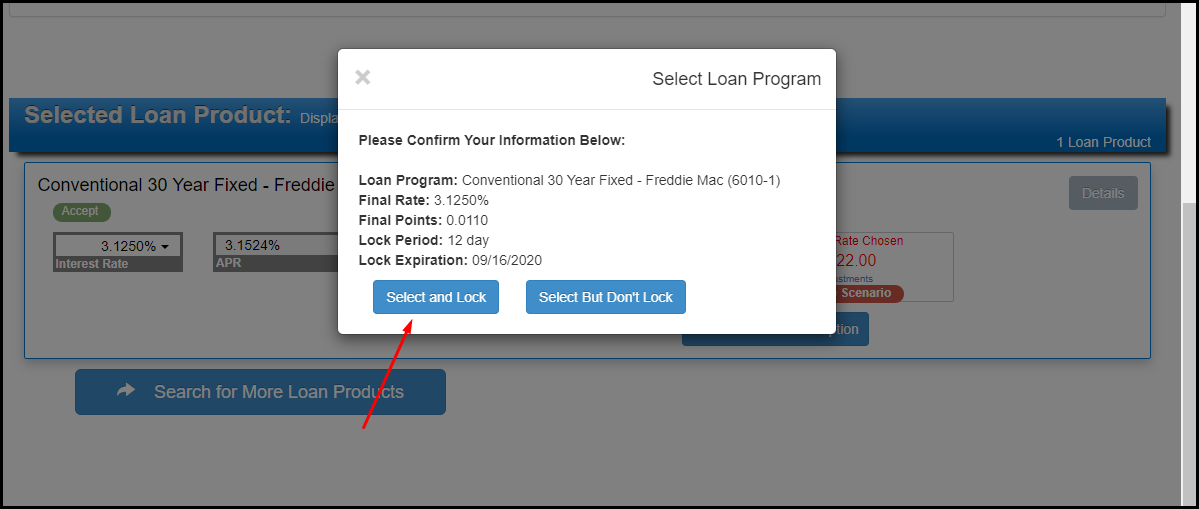

How do I lock a loan?

You can lock a loan fast and easy. We have listed the steps below as well as screenshots in order to better depict the process.

1. Log in to DirectWare

2.  Select the loan you wish to work on in the search Loans area of the Landing page header. You can search by loan number, by borrower first or last name (or use both), or use a partial name. There is also an “Advanced Search†option available to the right of the search box.

3. Click on “Loan Selection†from the menu on the left.

4. Once you’ve filled out all the necessary information click on “Search for Loan Productsâ€.

5. Once you’ve found your loan product click on “Select this Product Optionâ€.

6. If everything looks fine click “Select and Lockâ€

Also follow this link to view our rate lock policies and procedures here.

This post was last updated on 9/04/2020.Â

How late can I lock loans?

Loans may be locked in DirectWare® at the current day’s price until 1:00 a.m. Mountain time, the following day unless markets are going through a dramatic change.

Also follow this link to view our rate lock policies and procedures here.

This post was last updated on 9/04/2020.Â

What are your rate lock periods?

Direct Mortgage Corp. generally provides rate lock periods of 12, 30, and 60 days. However, other rate lock periods may apply for specific loan programs.

Also follow this link to view our rate lock policies and procedures here.

This post was last updated on 9/04/2020.Â

Can I change a loan program for an existing lock?

Yes. You can do this through DirectWare using the following clickpath: Log in >> Choose your desired loan by double-clicking the loan in the “Recent Borrowers†column on the left OR by entering the borrower’s name or the loan number into the “Loan Search on the left and clicking “Findâ€. A list of search results will appear. Choose your loan by double clicking the correct entry >> You will be taken to “Loan Choices†>> click “Locked†located in the row of your desired loan program (alternately, you can click the date next to “Loan Expirationâ€) >> click the “Change Interest Rate†button at the bottom of the window that opens >> A message will alert you that the lock will be priced as of today’s date. If you wish to proceed, click “OK†>> Click the YSP corresponding to your desired rate >> Review the rate and YSP after all the adjustments (look at the row that says “Total Rate with Adjustments†>> click “Update Lock†button.

What is your policy on rate lock expirations?

Loans must be closed and funded by the rate lock expiration date. Loans not closed and funded by the expiration date are subject to re-pricing.

Also follow this link to view our rate lock policies and procedures here.

This post was last updated on 9/04/2020.Â

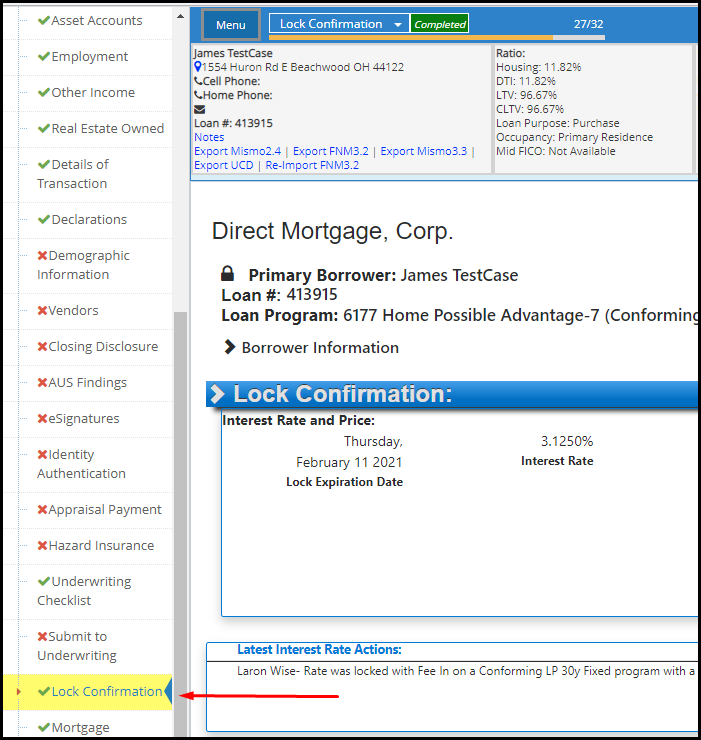

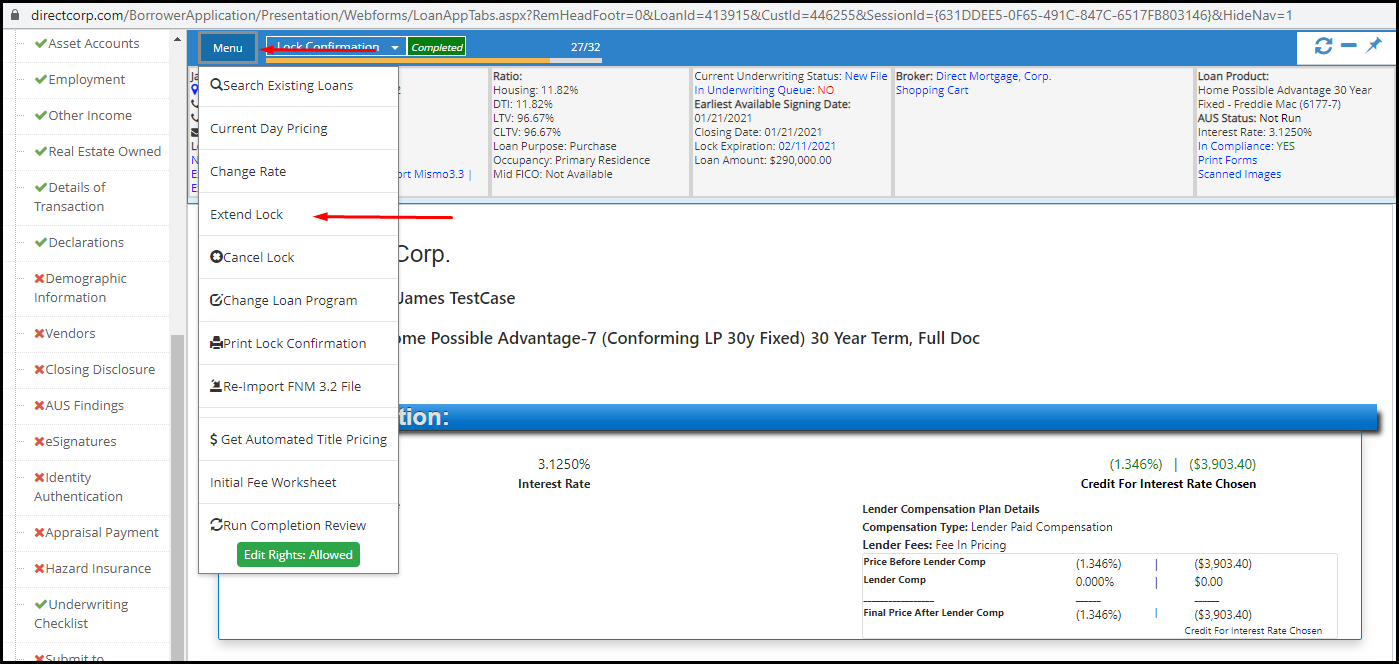

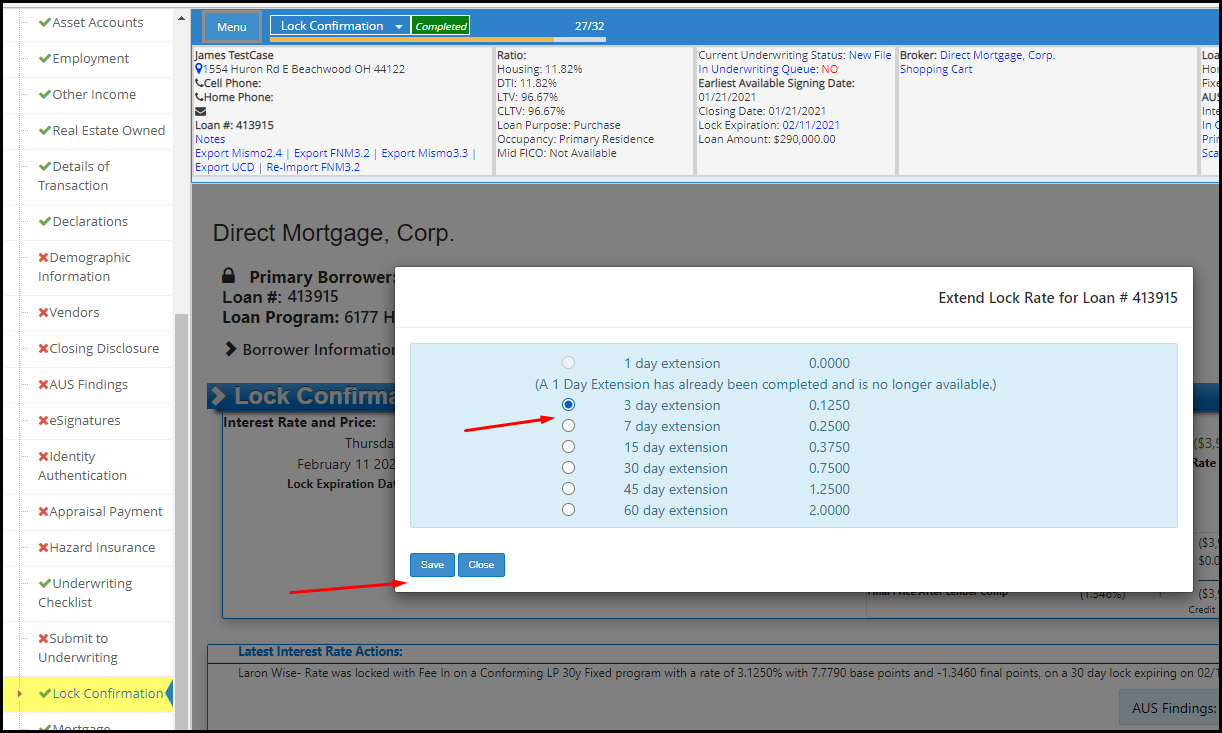

Do you offer rate lock extensions?

Yes, we do offer rate lock extensions. You can do this through the DirectWare platform. We have listed the steps below.

1. Log into DirectWare® at www.DirectCorp.com/Sitelogin/

2. Select the loan you wish to work on in the search Loans area of the Landing page header. You can search by loan number, by borrower first or last name (or use both), or use a partial name. There is also an “Advanced Search†option available to the right of the search box.

3. After opening the loan look to the side menu and find Lock Confirmation then click it.

4. Once the page loads locate the thumb menu on the loam page towards the header.

5. Once the menu opens click on Extend Lock and leave whatever notes are necessary.

6. Select how long you wish to extend the lock (extension prices will be listed) >> click “Saveâ€.

This post was last updated on 9/09/2020.Â

Can I change the interest rate on an existing lock?

Yes. You can do this through DirectWare using the following clickpath: Log in >> Choose your desired loan by double-clicking the loan in the “Recent Borrowers†column on the left OR by entering the borrower’s name or the loan number into the “Loan Search on the left and clicking “Findâ€. A list of search results will appear. Choose your loan by double clicking the correct entry >> You will be taken to “Loan Choices†>> Click “A Select a Loan Program†>> The loan program list will appear >> Enter your scenario criteria in the “Loan Search Criteria†portion of the Loan Choices screen if wanted and click “Submit†>> The scenario will run and loan programs will appear >> click “Select†located in the row of your desired loan program >> a message will appear. Choose “Select Loan – I’ll Process Myself†or “Select Loan – Process for Meâ€>> a message will appear stating that “Your Loan Program Has Been Selected†and ask you if you want to submit your loan to underwriting >> Select “Yes†or “No†>>

The “Loan Program†description in the upper right-hand corner should now be updated with the new loan program information >> Click on “Lock†next to where it says “Accept†(green circle with white check mark) >>

Message will appear asking if you want to change the locked loan program >> Click “Proceed†or “Cancel†>> a message will ask you if you want to submit your loan to underwriting >> select “No†>> The Lock Screen will open behind the Loan Choices screen. Minimize the Loan Choices screen so that you can see the Lock Screen. >> Click the YSP corresponding to your desired rate >> Review the rate and YSP after all the adjustments (look at the row that says “Total Rate with Adjustments†>> click “Update Lock†button.

Can I re-lock my loan after my original lock has expired?

Yes. You can do this through DirectWare using the following clickpath: Log in >> Choose your desired loan by double-clicking the loan in the “Recent Borrowers†column on the left OR by entering the borrower’s name or the loan number into the “Loan Search on the left and clicking “Findâ€. A list of search results will appear. Choose your loan by double clicking the correct entry >> You will be taken to “Loan Choices†>> If the loan has not been selected yet, select the loan by clicking “Select†in the row of the loan you have locked. If you have already selected the loan, the click on “A Select a Loan Program†at the top of the page >> Click “Locked†in the row of the loan you have locked >>

The “Rate Lock Request†screen will open >> Scroll to the bottom of the page >> Click on the “Re-Lock†button.

A message will appear stating that you will be subject to worse case pricing, meaning that the lock will be priced at either the original day’s lock price or today’s lock price, whichever is higher. If you want to proceed, click “OK†>> From within the “Rate Lock Request†window, click the YSP corresponding to your desired rate >> Review the rate and YSP after all the adjustments (look at the row that says “Total Rate with Adjustments†>> Scroll to the bottom of the page and click the “Update Lock†button >>

A message will appear asking you to confirm that you want to lock the loan at the selected rate. If you have selected the correct amount, then click “OK†>> The loan is now re-locked.

Do you offer contract processing services?

Yes. Contract processing is available through our 1Processing service. Loans processed through 1Processing that are also underwritten by Direct Mortgage will receive priority underwriting. Go to 1Processing.com for more information.

This post was last updated on 9/01/2020.Â

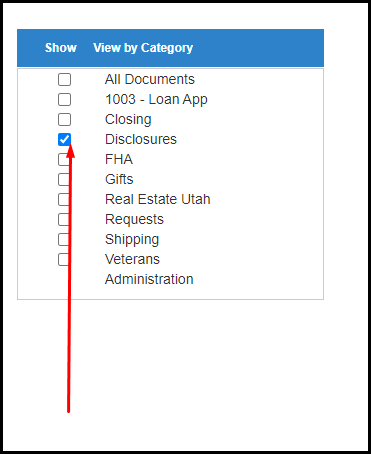

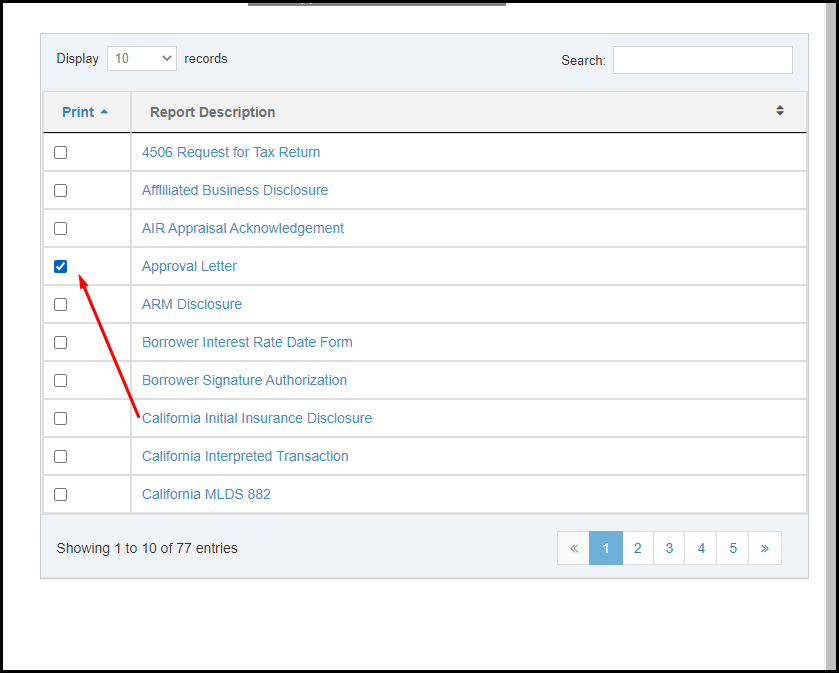

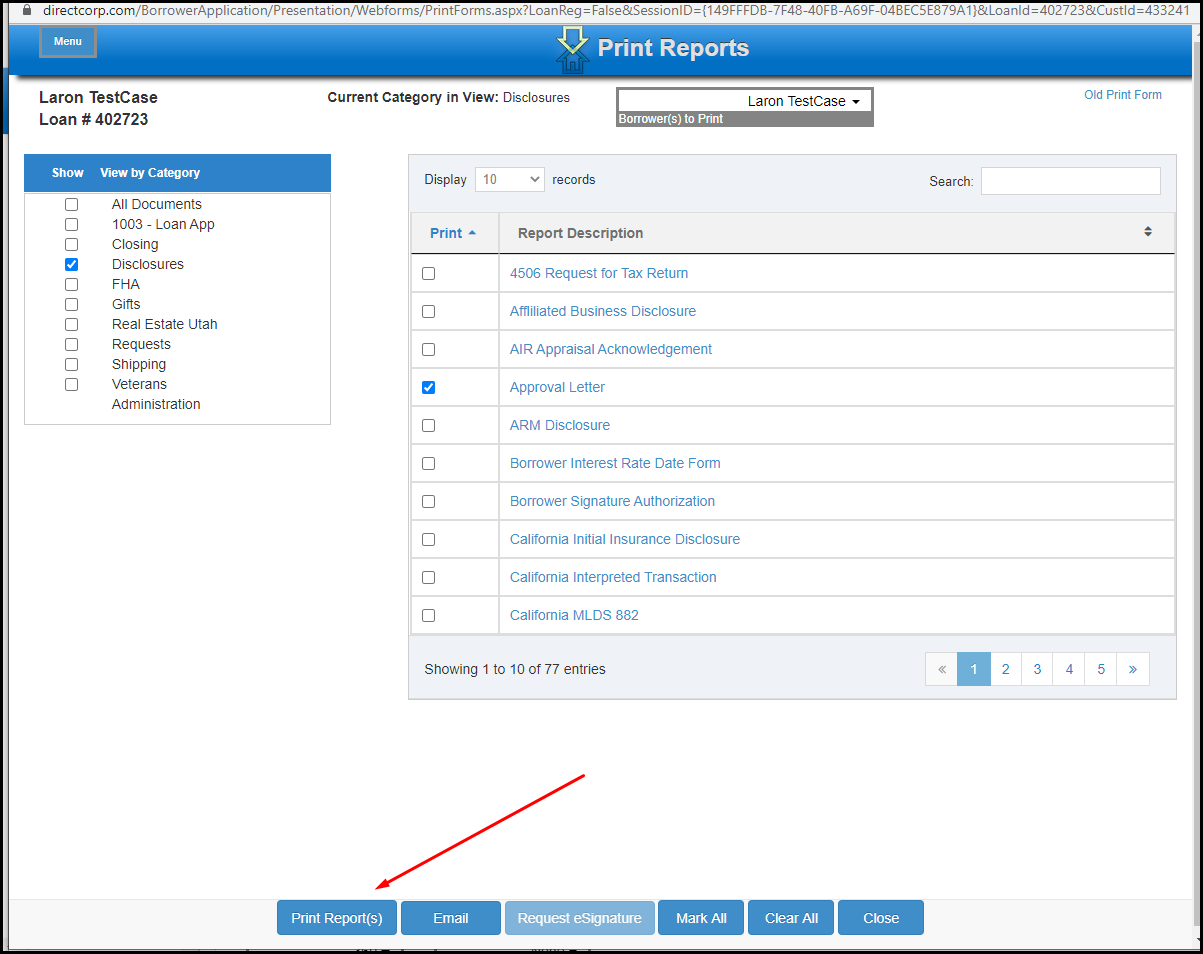

Is there a way to print out a pre-approval from DirectWare that can be shown to a realtor?

Printing a Pre-Approval is fast and simple. Below are the steps needed in order to do so.

1. Select the loan you wish to work on in the search Loans area of the Landing page header. You can search by loan number, by borrower first or last name (or use both), or use a partial name. There is also an “Advanced Search†option available to the right of the search box.

2. You will be taken to “Loan Summary†page where you then can select the “Print Forms†hyperlink inside of the headerâ€

3. Check the box next to “Disclosures†on the left side of the screen

4. Check the box next to “Approval Letterâ€

5. Lastly on the bottom of the page click on the button that says “Print reportsâ€. This will open a PDF version of the file where you can either save or print.

This post was last updated on 9/10/2020.Â

What is the hazard loss payee name and address (Mortgage Clause)?

Direct Mortgage, Corp.

Its Successors and/or Assigns

Loan #:

6955 S Union Park Center, Suite 540

Salt Lake City, UT 84047

This post was last updated on 9/01/2020.Â

What is the address for a closing protection letter (CPL)?

Direct Mortgage Corp.

6955 S. Union Park Center, Suite 540

Salt Lake City, Utah 84047

This post was last updated on 9/01/2020.Â

What is Direct Mortgage's FHA Lender ID?

FHA # 1173900006

This post was last updated on 9/01/2020.Â

What is Direct Mortgage's VA Lender ID?

VA # 9751390000

This post was last updated on 9/01/2020.Â

What if my username is not working?

Click here and then insert your email. Your username will be sent to your email if the email exists in our system.

This post was last updated on 9/01/2020.Â

What if my password is not working?

If you can receive html-formatted emails:

- Click here and then insert your email.

- An email will be sent to you with a link to create a new password.

- Click on the link.

- A browser window will open asking you to enter your new password twice (the second time is for confirmation).

- Click “Create new passwordâ€.

- The screen will now say “Please login to DirectWareâ€. Click on the link (“DirectWareâ€). Login using your new password.

OR, If you have a text-only (non-html) email account:

- Click here and then insert your email.

- An email will be sent to you with a link to create a new password.

- Return to the browser window where you entered your email address and click the link at the end of the line that states: “Once you have your reset code, you can enter it here.â€

- Enter the passcode included in the email and click “Submitâ€.

- A browser window will open asking you to enter your new password twice (the second time is for confirmation).

- Click “Create new passwordâ€.

- The screen will now say “Please login to DirectWareâ€. Click on the link (“DirectWareâ€). Login using your new password.

This post was last updated on 9/01/2020.Â

What happens when a rate lock expires on the weekend or a holiday?

If a lock expires on a weekend or holiday, the expiration should automatically roll to the next business day. There is always the option to use the 1 day free rate lock extension. The steps to do so are below.

Also follow this link to view our rate lock policies and procedures here.

1. Log into DirectWare® at www.DirectCorp.com/Sitelogin/

2. Select the loan you wish to work on in the search Loans area of the Landing page header. You can search by loan number, by borrower first or last name (or use both), or use a partial name. There is also an “Advanced Search†option available to the right of the search box.

3. After opening the loan look to the side menu and find Lock Confirmation then click it.

4. Once the page loads locate the thumb menu on the loam page towards the header.

5. Once the menu opens click on Extend Lock and leave whatever notes are necessary.

6. Select how long you wish to extend the lock (extension prices will be listed) >> click “Saveâ€.

End of Explanation

Last updated 1/12/21

eSign Instructions

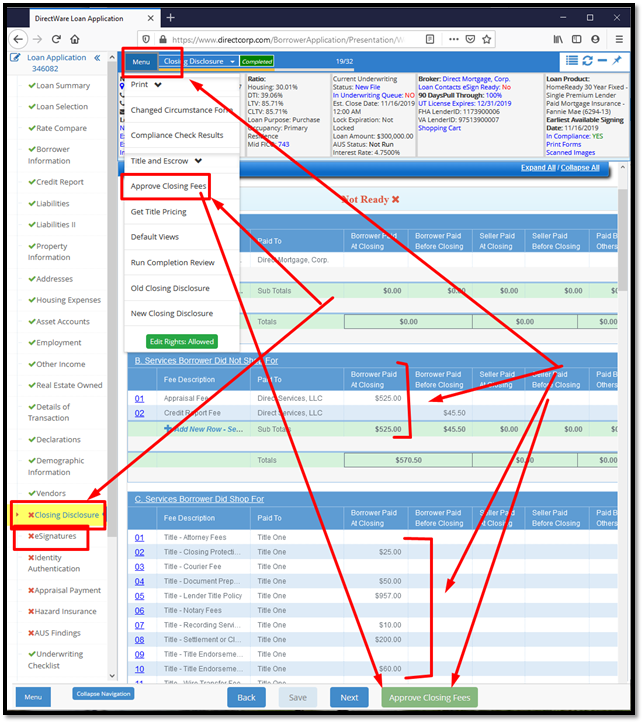

- Approve Closing Fees. Before sending the Initial Disclosures, the Loan Officer must review and approve their closing fees. They do this by reviewing the Closing Disclosure in the DirectWare After their review, they click the “Approve Closing Fees†button on the footer (or in the menu) of the Closing Disclosure.

- For Initial Disclosure purposes, the Closing Disclosure and the Loan Estimate are treated as being the same thing, i.e. the Loan Estimate is the Closing Disclosure.

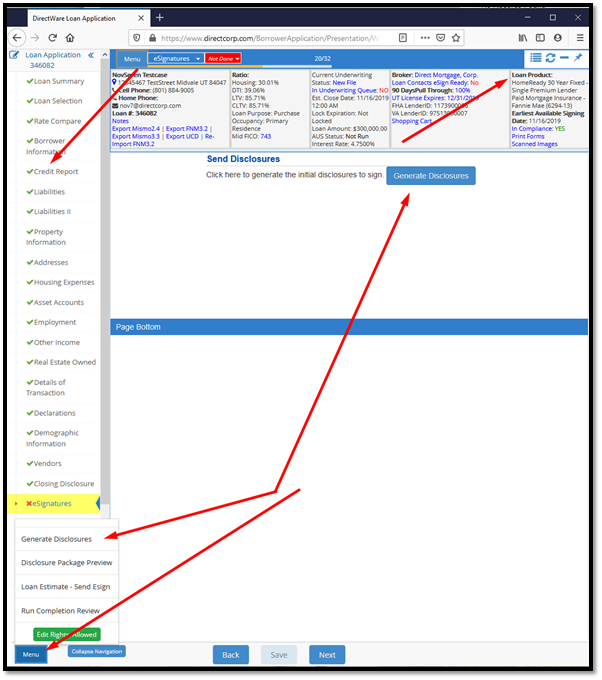

- Generate eSign Disclosures. After approving their fees, the loan officer navigates to the eSignatures page, and simply clicks the button to generate disclosures. eSign emails and disclosures are generated by clicking this button.

- Best practices. It is always best for the loan officer to pull a full credit report, and select a loan product in DirectWare before sending disclosures. This is not required, but there underwriting requirements that can be added to the eSign process (i.e. credit explanations), and loan specific product information used in underwriting that can be automated if these steps are completed before disclosing. If the loan officer misses this the first time, they can always revisit the eSignatures page after completing the credit report and loan selection steps) and then click to “Generate Disclosures†option again (found in the menu).

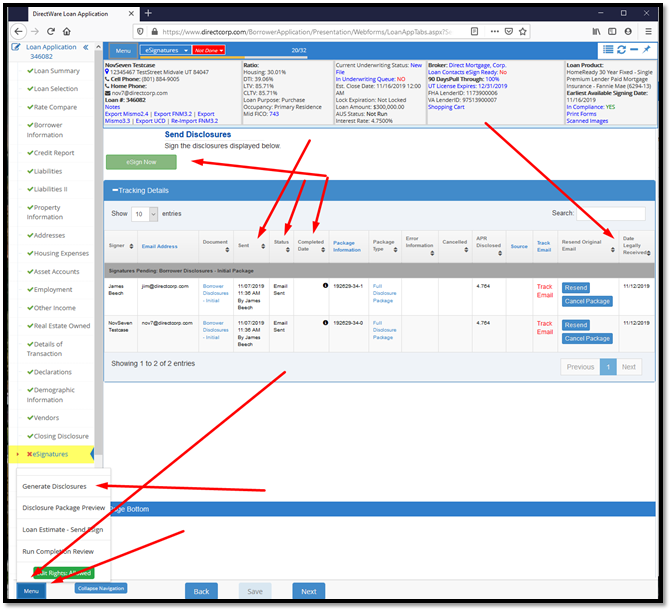

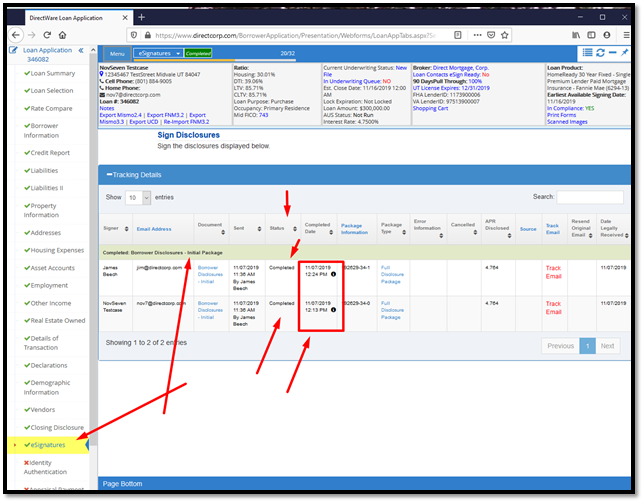

- After disclosures are sent, the loan officer can track the current status of all eSignature Packages right from the eSignatures screen.

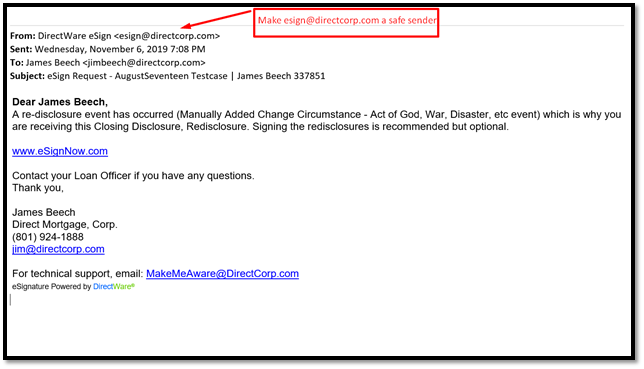

- Safe Sender. eSign Email Sender: esign@directcorp.com.

- Make sure the person receiving the eSign request makes us as a “safe sender†to avoid the email going into the Junk Mail folder.

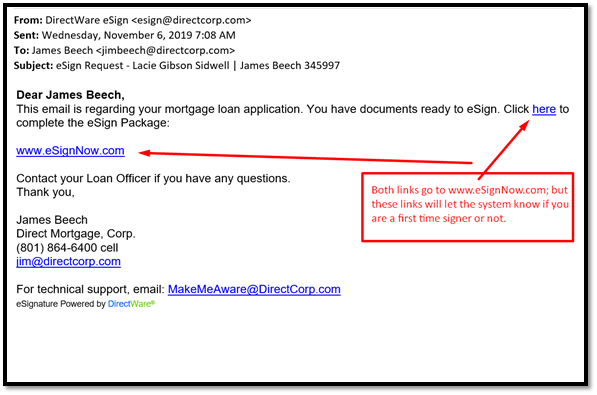

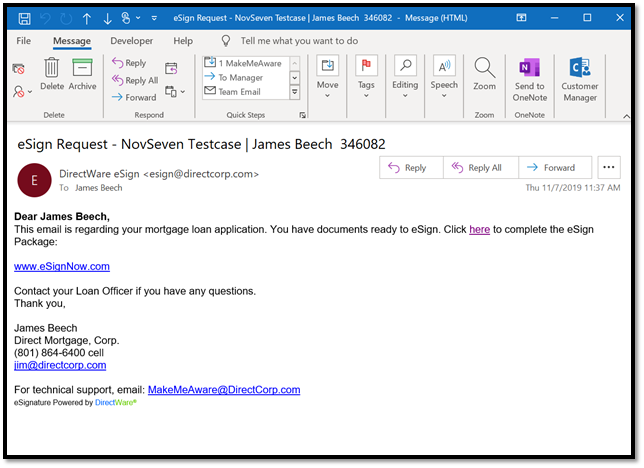

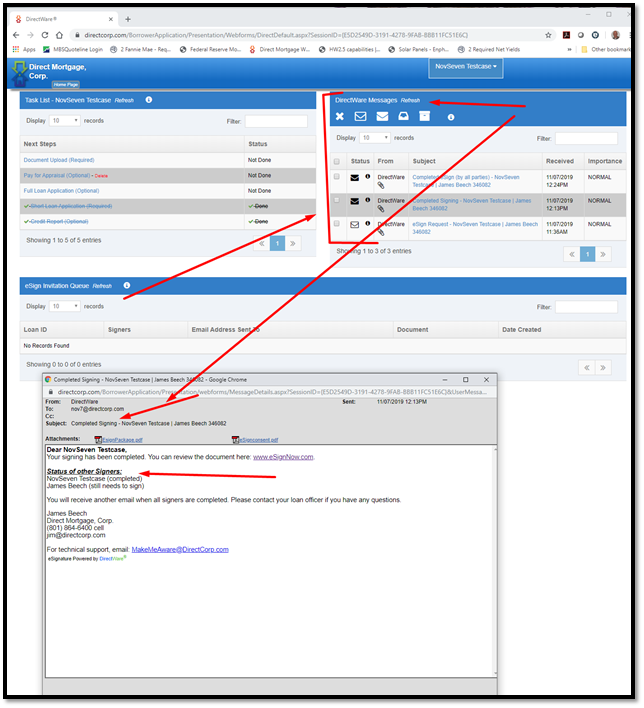

- Email receipt. The Signer (eSign receiver) will receive an email like the one shown in the screen shot below.

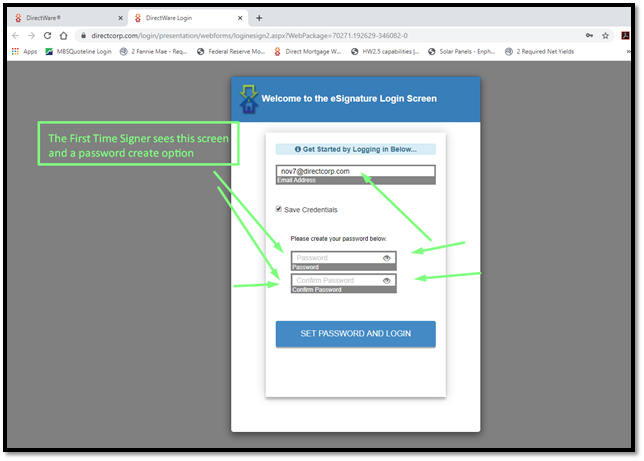

- First Time Signer. Click the link to set your password.

- Returning Signer. Enter your password created previously.

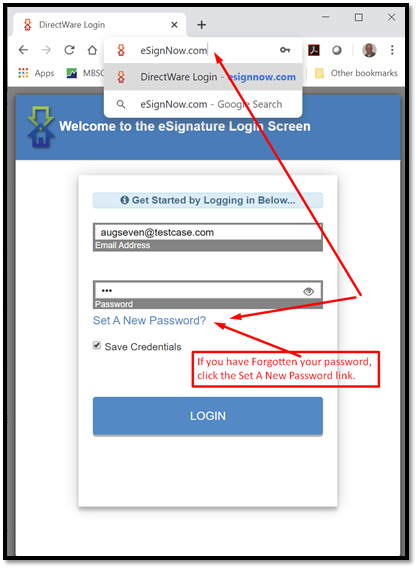

- Forgot Password. Simply click the link to reset the password. Make sure that your loan officer set your cell phone correctly, to add an additional option to email, when resetting your password.

- eSignNow.com. If No Email is Received, simply use this website: www.eSignNow.com.

- There is no requirement to receive an email. But if you are a first-time user, you will need to use the forgot password function (use the Set A New Password link) to create a password.

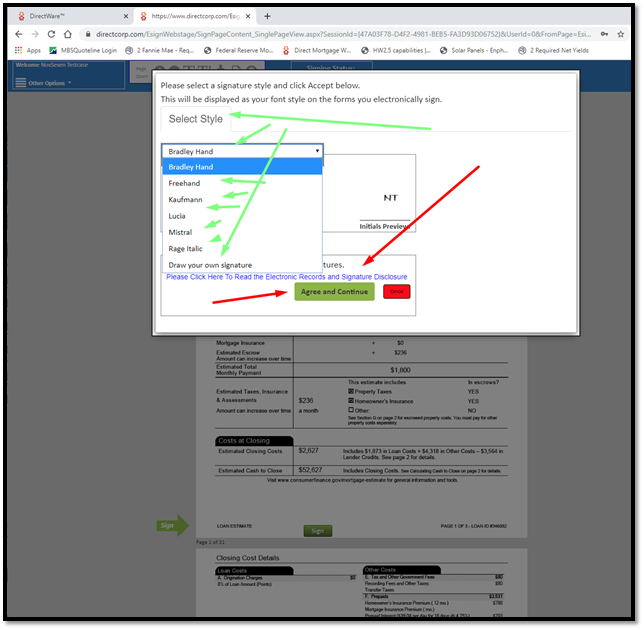

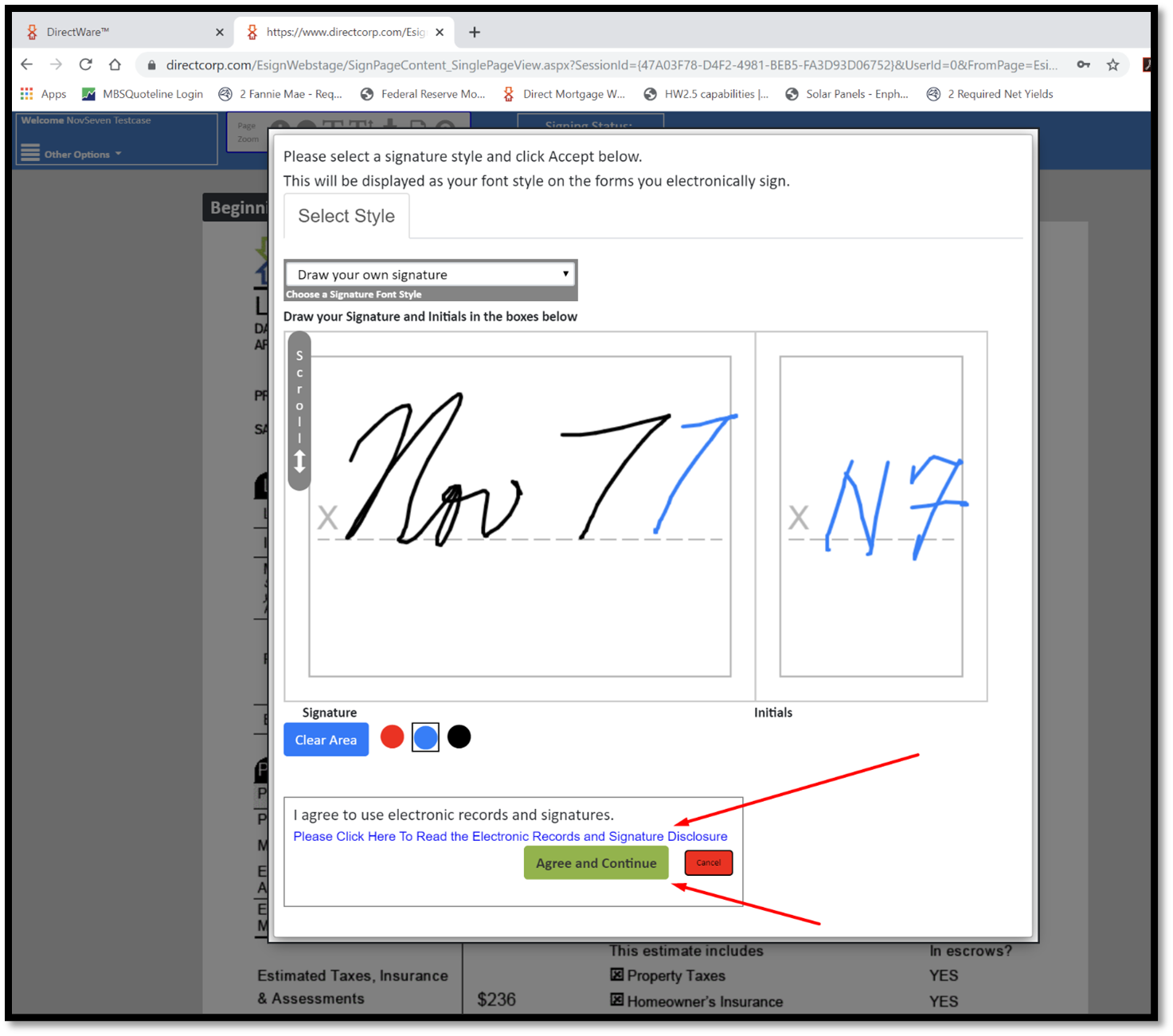

- Select a Signature Style and Agree to eSign Consent. During your first signing, you must first select a signature style to represent your signature. Then you must provide your eSign Consent. This allows you to eSign.

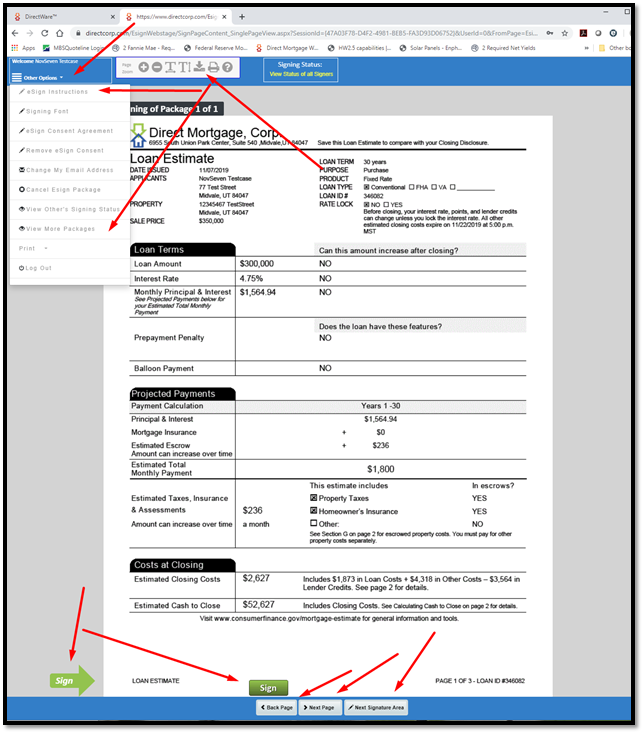

- Start signing. Either “Click with your mouse†the “Sign†tag, or use the “Space Bar on your keyboard†to eSign all of the documents. When you sign one page, the program will automatically skip to the next signing area. Or you can scroll upward or downward to any page.

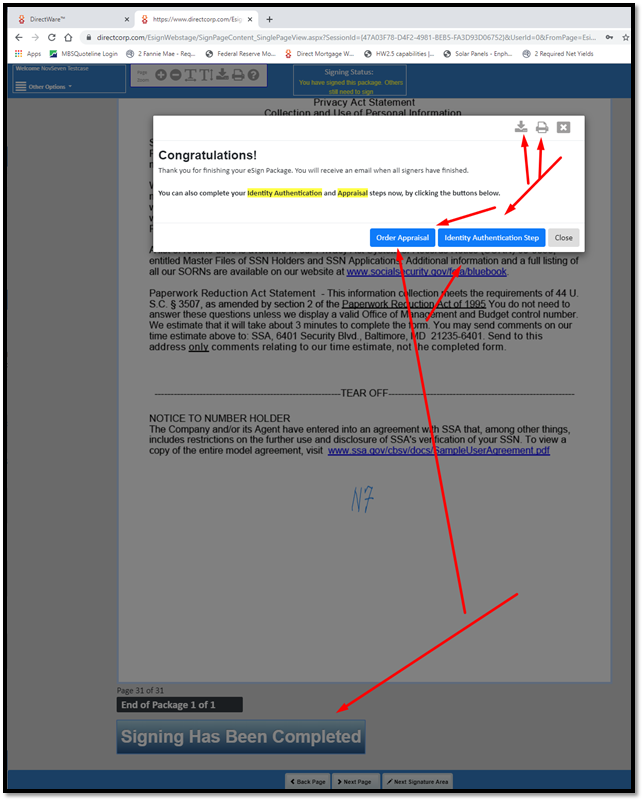

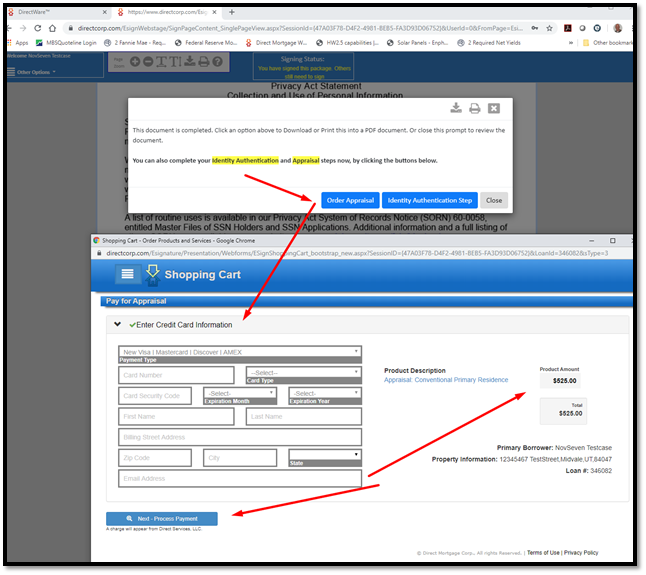

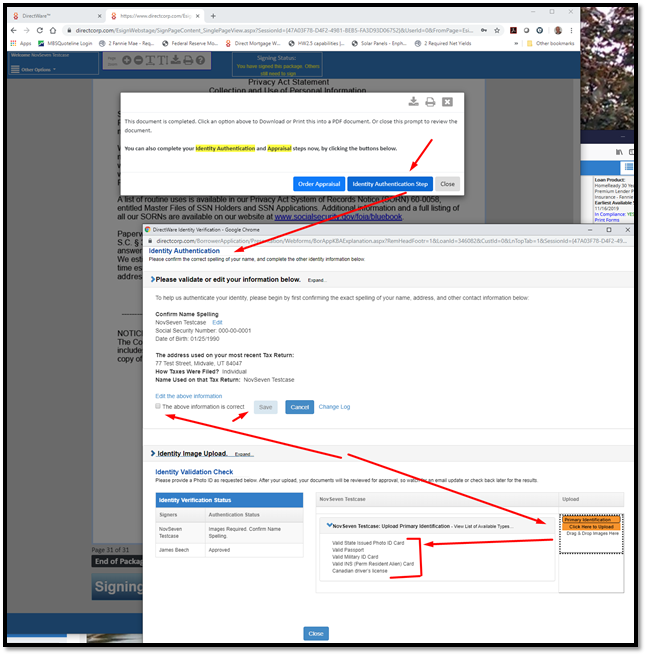

- Complete Signing. After signing the last required signature, you will be given an option to order the appraisal and to upload a Photo ID. These are optional (not required) at this stage, but will expedite your loan process if you complete them at this same time.

- Receive Signed Documents. To review your signed documents at any time, simply log back in to eSignNow.com and select the page you want to review. You can then download a PDF from there.

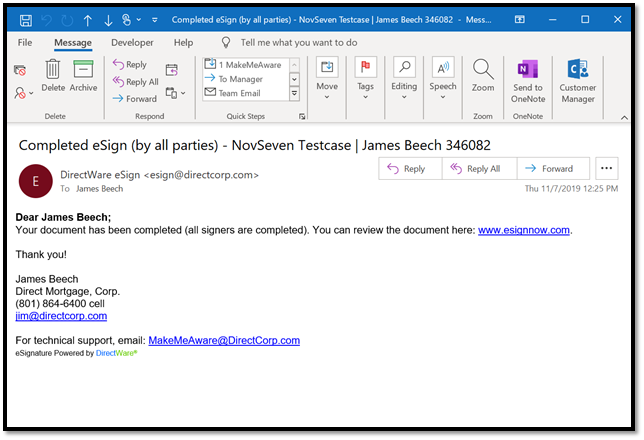

- Additionally, you will receive the following 3 emails for each eSign Package, as follows:

- 1) eSign Request. This is the invitation to eSign.

- 2) eSign Completed. This is the email you receive when you have completed signing. If you are the last person to sign a package then you won’t receive this email, but will receive the “all completed†email in place of this.

- 3) eSign Completed (all signers). This is the email you receive when all signers have completed signing.

- To download a PDF, you can either download right after completing the eSign, or follow the link and instructions given in the eSign Completed (all signers) completed email. Additionally, you don’t need an email to login to eSignNow.com at any time to review your packages – that are either signed or not signed.

- Underwriting and Automated Sign Off. Because DirectWare is integrated with our entire loan system, the underwriting conditions associated with these eSign documents are automatically signed off as the eSignatures are completed.

Following are the screenshots displaying each step above.

That’s it. Thank you!

Step 1

Approve Closing Fees. Before sending the Initial Disclosures, the Loan Officer must review and approve their closing fees. They do this by reviewing the Closing Disclosure in the DirectWare system. After their review, they click the “Approve Closing Fees†button on the footer (or in the menu) of the Closing Disclosure.

For Initial Disclosure purposes, the Closing Disclosure and the Loan Estimate are treated as being the same thing, i.e. the Loan Estimate is the Closing Disclosure.

Step 2

Generate eSign Disclosures. After approving their fees, the loan officer navigates to the eSignatures page, and simply clicks the button to generate disclosures. eSign emails and disclosures are generated by clicking this button.

Best practices. It is always best for the loan officer to pull a full credit report, and select a loan product in DirectWare before sending disclosures. This is not required, but there underwriting requirements that can be added to the eSign process (i.e. credit explanations), and loan specific product information used in underwriting that can be automated if these steps are completed before disclosing. If the loan officer misses this the first time, they can always revisit the eSignatures page after completing the credit report and loan selection steps) and then click to “Generate Disclosures†option again (found in the menu).

Step 3

Tracking. After disclosures are sent, the loan officer can track the current status of all eSignature Packages right from the eSignatures screen.

Â

Â

Step 4

Safe Sender Screen Shot. eSign Email Sender: esign@directcorp.com.

Make sure the person receiving the eSign request makes us as a “safe sender†to avoid the email going into the Junk Mail folder.

Step 5

Email receipt Screen Shot. The Signer (eSign receiver) will receive an email like the one shown in the screen shot below.

- First Time Signer. Click the link to set your password.

- Returning Signer. Enter your password created previously.

- Forgot Password. Simply click the link to reset the password. Make sure that your loan officer set your cell phone correctly, to add an additional option to email, when resetting your password.

Step 6

www.eSignNow.com. If No Email is Received, simply use this website: www.eSignNow.com.

There is no requirement to receive an email. But if you are a first-time user, you will need to use the forgot password function (use the Set A New Password link) to create a password.

Step 7

Select a Signature Style and Agree to eSign Consent. During your first signing, you must first select a signature style to represent your signature. Then you must provide your eSign Consent. This allows you to eSign.

Step 8

Start signing. Either “Click with your mouse†the “Sign†tag, or use the “Space Bar on your keyboard†to eSign all of the documents. When you sign one page, the program will automatically skip to the next signing area. Or you can scroll upward or downward to any page.

Step 9

Complete Signing. After signing the last required signature, you will be given an option to order the appraisal and to upload a Photo ID. These are optional (not required) at this stage, but will expedite your loan process if you complete them at this same time.

Step 10

Receive Signed Documents. To review your signed documents at any time, simply log back in to www.eSignNow.com and select the page you want to review. You can then download a PDF from there.

Additionally, you will receive the following 3 emails for each eSign Package, as follows:

1)Â eSign Request. This is the invitation to eSign.

2) eSign Completed. This is the email you receive when you have completed signing. If you are the last person to sign a package then you won’t receive this email, but will receive the “all completed†email in place of this.

3) eSign Completed (all signers). This is the email you receive when all signers have completed signing.

To download a PDF, you can either download right after completing the eSign, or follow the link and instructions given in the eSign Completed (all signers) completed email. You don’t need an email to login to www.eSignNow.com at any time to review your packages – that are either signed or not signed.

The Borrower View screen shot below is for partially completed packages, and showing where the eSign messages can be found – in addition to the borrower’s email inbox. This screen shot was accessed by a borrower login at www.DirectCorp.com.

Step 11

Underwriting and Automated Sign Off. Because DirectWare is integrated with our entire loan system, the underwriting conditions associated with these eSign documents are automatically signed off as the eSignatures are completed.

End of Explanation.

Are we automatically approved to do VA loans when we sign up?

While waiting for sponsorship approval, Direct Mortgage, Corp. (DMC) may allow you to close up to 2 VA loans. Brokers are not automatically approved to do VA loans upon sign-up approval with DMC.

The process to become VA Sponsored by DMC is simple:

1) Send us a $100.00 check, made payable to the Veterans Administration.

2) Mail to: Direct Mortgage, Corp., Attn: VA Sponsorship, 6955 S. Union Park Center, Suite 540, Midvale, Ut 84047. We will forward the required request form to the VA and notify you when sponsorship is approved.

Annual VA Renewal: The VA requires you to renew the sponsorship each year. This is done by sending us a payment each year. Currently, the renewal amount is $100.00.

End of Explanation.